Human resources and marketing are the two areas where the majority of companies spend the most of their money. The proactive strategy taken by VCs entails close collaboration with their portfolio firms to thoughtfully plan and get ready for these critical areas well in advance, ensuring they are well-equipped to handle possible obstacles.

Highs and lows are unavoidable since markets are always changing. To assist the company’s founders in overcoming any unique difficulties that may arise, the investors keep in close contact with them. The founders also continue to engage with and seek assistance from their investors’ extensive networks, which span numerous nations and industries.

Based on a structure they hope will keep businesses honest throughout all phases of the start-up lifecycle and help them through challenging times by prioritising important areas of emphasis, VCs have continued to work alongside their portfolio in light of recent events over the previous 12 months.

Here are a few steps that venture capitalists have taken to control the financial parameters, including burn and runaway, of the firms in their portfolio.

Closely works with founders

3one4 Capital works with its founders to plan and actively manage financial metrics including burn and runway. According to Nruthya Madappa, Partner, 3one4 Capital, “These are critical aspects we help them monitor and gain control over on an ongoing basis regardless of the macro scenario.”

The VC firm drives continuous, collaborative financial planning across its portfolio, to explore and capture cost optimisation and business model efficiencies to help founders make their companies more resilient.

Encourages concentrating on core businesses

Kae Capital asks that its portfolio companies aggressively concentrate on their key competencies and start reducing costs in non-core competencies where there is no significant PMF (Product Market Fit). In some circumstances, “we suggest that they search for bridge rounds as well,” according to Kae Capital Partner Gaurav Chaturvedi.

Vishesh Rajaram, Managing Partner of Speciale Invest, continued, “Startups occasionally might have to let go of their employees as well. We advise founders to spend all of their remaining funds only on endeavours that advance technology and company, which will lower risk, boost chances of success, and help them raise additional money.”

Run a special program and connect with the right partners

Inflection Point Ventures has set up unique initiatives like a ‘Lets Grow Start-up’ program for deep engagement with 4-5 identified experts from various domains who work closely with its portfolio companies advising on strategy and have a regular check on burn and runway.

Apart from the cash conservation and management exercise on a case-to-case basis, “we do assist companies in connecting to right partners (like other VCs, RBF companies) for intermediate financing arrangements,” stated Ankur Mittal, Co founder, Inflection Point Ventures.

Look for a M&A target

During these times, in addition to locating funding sources, cost reduction and—most importantly—standing by the founders when things become rough could mean the difference between success and failure. “Our portfolio management team gets involved when it becomes crucial for the start-up to hunt for an M&A target to sustain or increase shareholder value. Several of our companies, including Supr Daily, Belita, and AHA Taxis, have been acquired throughout the years, giving investors an exit,” as per Lead Angels Founder and CEO Sushanto Mitra.

Recommend being creative, freezing new experiments, & prioritising profitability

According to BEENEXT, it keeps in close contact with its founders to assist them in overcoming any unique difficulties that may emerge. “For instance, we advise being creative to lessen the burn if the firm has less than 18 months of runway and is still attempting to identify its Product Market Fit. Prepare for a hard reset with just the core staff and be ready for the worst-case scenario,” advised Chinmaya Saxena, Partner – Community Strategy, BEENEXT.

But if the start-up has already achieved Product Market Fit and has a longer runway than 18 months, the priority should be finding new funding as quickly as possible. “We advise doubling down on the primary product’s monetisation while halting any new experiments and hires. Additionally, it is essential for these start-ups to provide a clear route to profitability, perhaps by securing longer revenue contracts or subscriptions,” Sexena said.

On the other hand, if start-ups have less than 18 months of runway but have not found their Product Market Fit, efforts need to be on low-cost Product Market Fit discovery by reducing burn and preserving runway for as long as possible. “If the start-up has achieved Product Market Fit and has more than 18 months of runway, then they need to prioritize profitability over growth by doubling down on channels that are working well and cutting down on low ROI experiments,” emphasised Saxena.

Sujata is an engineering graduate and has done her Post Graduation in Human Resource Management. She has a deep interest in startups, venture capitalists & technology. She can be reached at [email protected].

If you’re not already using artificial intelligence (AI) to enhance your digital strategy, fear not. Tug’s Elliot Gray has you covered.

Artificial Intelligence (AI) is revolutionizing the media industry. It’s opened up a huge range of new possibilities for digital marketers, helping them gain competitive advantages and engage with customers in new and exciting ways.

Here, we cover seven things digital marketers can do with AI to speed up workflows, boost ROI on ad campaigns, and more.

1. Automate repetitive tasks

While the role of the digital marketer is forever changing, there are some repetitive admin tasks we haven’t been able to shake – until now. Sending emails, posting on social media, conducting research. AI can automate all of these, freeing up time for marketers to focus on higher-value work.

Robotic Process Automation (RPA) software like Zapier can integrate with 5,000 apps and platforms to create automated workflows, automating the process of lead-generation campaigns, for example.

2. Create personalized content

AI can also be used to create more personalized content. Businesses have utilized this for many years. In 2016, Starbucks used predictive analytics to create customized emails by leveraging loyalty card and mobile app data. By analyzing data about consumer behavior, AI can help marketers better understand what kinds of content are most likely to resonate with the audience they’re trying to reach.

3. Conduct audience research

Conducting audience research can be tedious, but AI can speed it up by collecting and analyzing data about potential customers. It can also support marketers in identifying new audience segments they might not have considered before.

At Tug, we use ChatGPT to help identify new audience interests to target on Meta when planning a campaign by feeding the platform as much relevant information about the company and its products or services as possible, then asking it to provide around 50 options. Admittedly, it can spit out a lot of nonsense, but by asking for a large list of options, you have a better chance of finding hidden gems.

4. Improve customer service

Digital marketers can’t be on standby for their clients all hours of the day. By using chatbots, businesses can provide their customers with 24/7 assistance, even outside regular business hours.

Chatbots can answer FAQs or give product recommendations. Implementing a chatbot can help reduce the time employees spend answering simple questions. When something more complex comes up that the chatbot can’t answer, it can escalate the issue to an actual human.

5. Analyze data

AI can assist digital marketers with collecting and organizing data from various sources, reducing the time spent on obtaining and arranging the data, as well as making the process more streamlined overall.

If we take something like ‘sentiment analysis’ as an example, a company might use AI tools to gauge customer attitudes toward a specific brand, product, or ad campaign. This can be done by reviewing social media posts, reviews, and other online feedback in order to help understand public perception and adjust accordingly.

6. Analyze performance

Even better, AI can be adopted to analyze the performance of campaigns across multiple channels. By analyzing data from multiple sources, marketers can better understand how each channel contributes to overall success and adjust their strategies accordingly.

7. Predictive analytics

AI can predict future trends and consumer behavior more accurately than manual analysis. Predictive analytics uses machine learning algorithms to analyze large customer datasets and identify patterns that indicate future trends. For example, AI can determine which products or services are likely to soon become more prevalent, or which customers could be more likely to remain loyal customers.

8. Automate media buying processes

Through automation, AI can make the media buying process more efficient. By sifting through consumer behavior and market trends data, AI can help businesses find the best deals for their media campaigns, preventing them from overspending on ad buys. For example, AI can identify the best times and channels to run ads in order to maximize their reach while saving on costs.

Getting these answers can help determine if they are right for you and your money.

Because the finance world can be both complex and overwhelming, you need to know the right questions to ask to vet a financial adviser and determine if you two are a good match.

“Depending on the type of client, most should first think of what they are looking for in an adviser before they even meet,” says Nicholas Bunio, a certified financial planner with Retirement Wealth Advisors. “Do you want an adviser to just do retirement planning, or someone who can do retirement planning, plus estate planning, and insurance planning? Or are you looking for someone who invests money? Maybe you are looking for someone to manage your investments, or someone who sells life insurance, annuities or long-term care?,” he explains. (Looking for a new financial adviser? This tool can match you to an adviser who meets your needs.)

Then schedule a face-to-face meeting. This is the best time to not only convey your own personal financial standing and what you want from an adviser, but also your lifestyle, employment history, hopes and dreams for the future — and what you expect to get out of the relationship.

Here are the 9 most impactful questions you can ask in that first meeting with your prospective financial adviser:

1. Are you a fiduciary?

When it comes to financial advice, the term fiduciary means quite a bit; determining whether or not the financial planner you’re considering working with is one can be one of the most important questions you can ask.

First, what is a fiduciary? In simple terms, a fiduciary is an adviser who is required by law to work with your best interest in mind when it comes to managing your assets. While not all financial advisers follow these guidelines, those who do are most often known as registered investment advisers, or RIAs. By design, RIAs meet these requirements. Certified financial planners, also known as CFPs, may also carry this status, but it’s best to ask any adviser if they’re a fiduciary first to find out. (Looking for a financial adviser who is also a fiduciary? This tool can match you to an adviser who meets your needs.)

2. What are your qualifications/credentials?

Certifications carry a lot of weight in the world of financial planning. When you’re researching the advisers in your area, you’ll probably see the various credentials tacked to the ends of their profiles and email signatures. Here are just 10 of the most common credentials to look out for and a little about what they mean:

Common credentials and designations for financial advisers

Certified financial planner (CFP)®: This certification is backed by the Certified Financial Planner Board of Standards, also known as the CFP Board. If you’re looking for an adviser with expertise in financial planning, taxes, insurance, estate planning and retirement saving, a CFP may be the way to go. CFPs are also required to be a fiduciary of your assets, which in short means they are required to work in your best interest when it comes to managing your money.

Chartered financial analyst (CFA)®: This subsect is recognized by the CFA Institute and ensures your adviser has passed exams covering topics such as accounting economics, ethics, money management and security analysis. For some context on the exclusivity of the CFA credential; more than two million candidates have taken the Level I exam since its inception in 1963, with 291,500 candidates going on to pass the Level III exam, according to Investopedia.

Certified fund specialist (CFS): Advisers with a CFS certification have been certified by the Institute of Business & Finance (IBF) for their proficiency in working with mutual funds. Those who hold this title are qualified to become accountants, bankers, brokers, money managers, personal financial advisers, and various other financial industry professionals. To maintain this credential, advisers with a CFS are required to recertify with 30 hours of education every two years.

Chartered financial consultant (ChFC): Issued by the American College of Financial Services, this designation ensures additional expertise in tax and retirement planning for special needs, wealth management, insurance and more. Continuing education requirements here is also 30 hours every two years with at least one hour in ethics.

Chartered investment counsellor (CIC): Started by the National Alliance for Insurance Education & Research in 1969, the CIC certification is designated for agency owners, producers, agents, brokers, as well as agency and company personnel who meet various requirements and who pass five of seven course exams on the following topics: personal lines, commercial casualty, commercial property, life and health, agency management, commercial multiline and insurance company operations.

Certified investment management analyst (CIMA): Financial consultants and investment advisers who achieve this credential from the Investments & Wealth Institute typically build their business around investments, risk assessment and portfolio management. This certification requires three years of industry experience, no record of ethical misconduct, a passing score on the qualifying course offered at Yale, the University of Pennsylvania or the University of Chicago, a passing grade on the exams offered by the Investments and Wealth Institute, and 40 hours of continuing education every two years to maintain.

Chartered market technician (CMT)®: Those with this credential from the CMT Association demonstrate an expertise in investment risk in portfolio management including quantitative risk and market research, and rules-based trading system design and testing. CMTs are additionally qualified to conduct research, author research reports, recommend trades and investment programs and trade their own accounts.

Certified public accountant (CPA): This is probably one of the more widely recognized credentials in public finance. CPAs are proficient in taxation auditing financial analysis and regulation, and meet both high professional and accounting standards. With tax season around the corner, this is a financial professional that may soon come in handy for just about all of us.

Personal financial specialist (PFS): This credential is issued by The American Institute of Certified Public Accountants (AICPA). Those with a PFS must hold an unrevoked CPA certificate, become a member of the AICPA and have at least two years of full-time teaching or business experience in personal financial planning.

Chartered life underwriter (CLU): If you’re looking for an expert in life insurance, estate planning, and business planning, financial professionals with a CLU might be for you. Often CFPs will add this credential to demonstrate this additional expertise.

It should be noted that these are only a fraction of the wide universe of potential credentials a financial adviser may carry. That said, these titles can also help decide if the adviser you are interviewing is a match for your financial needs.

Aside from certifications, you can also ask about their personal background. You may want to ask where they went to college or what degrees and credentials they attained while they were there.

Do a deeper dive on the financial adviser’s background

Plus, do a full background check. For starters, a good resource for background information on the brokers, brokerage firms, investment adviser firms and advisers you’re considering is a free tool from the Financial Industry Regulatory Authority (FINRA) known as BrokerCheck.

After searching for finance pro in your region (associations such as FPA or NAPFA have ‘find an adviser’ portal to help match someone with your needs), the BrokerCheck website can show more about their credentials and work history, as well as any previous legal disputes they may have encountered throughout their professional careers with their firms or clients.

3. What are your personal or firm values?

Knowing an adviser’s values or investment philosophy can either be a dealmaker or breaker for many of us. Does the firm engage in actively managing your funds or do they let automated tools do all the work? If they choose them on their own, how do they make their investment selections? Are their decisions based on choices that you feel comfortable with? Or do you get the sense that they are making random decisions?

Finding the right financial adviser for your personal ethics and background

Bunio says knowing whether the adviser you’re considering is on the same page as you ethically and demographically is highly important. Since you will be working closely with your financial adviser, likely over a long period of time, “it’s always good to find someone who works with your type of demographic, such as teachers, people 50+, spouses or LGBTQ+.”

4. Are you primarily a financial planner or an investment adviser?

By now, it probably comes as no surprise that there is more than one kind of financial adviser. Knowing the difference between the two most common — financial planners and investment advisers — is another way to help determine whether the adviser you are meeting with is right for you.

“Some advisers only do financial planning,” says Bunio. “Others do planning, but they must manage your investments. Others don’t do estate planning. Many want nothing to do with insurance and even recommend against buying it. Whether right or wrong, not all advisers are the same.”

Here are some key differences between the two:

Investment adviser

For starters, investment advisers typically specialize in securities and provide clients with data analysis to pick and manage their investments.. They also typically charge a fee to work with you and have a fiduciary responsibility to put your financial needs first. Investment advisers are also registered with the Securities and Exchange Commission (SEC) if they manage more than $100 million in combined client assets.

They can specialize in a wide range of financial advice, such as estate planning, retirement planning, investment management or taxes. This class of financial adviser often works with higher income levels.

Financial planner

The term financial planner is used as a wide brush in the world of financial advice. While many who fall into this category can be highly credentialed, the term financial planner doesn’t necessarily mean these individuals actually have any financial credentials.

While often used synonymously with the term financial adviser, a financial planner, much like its title, is primarily concerned with assisting with developing a financial plan for their clients. These can revolve around just about any aspect of a potential client’s financial wellbeing, including savings, college planning, retirement, taxes, insurance and estate planning.

5. What is your fee structure?

Knowing how your prospective financial adviser charges you for their services is likely one of the most important factors to consider. Do they charge a fixed fee, are they hourly, does their rate depend on how much money you have or will they charge you based on how much money they can help you earn?

For some background on this topic, and to help power your decision when you’re asking your adviser about the first place to look is fee structure.

Here are the five most common ways financial advisers charge their clients:

Percentage of assets under management: With this model, advisers charge fees based on your total amount of invested money, or assets under management (AUM). A typical fee is about 1%, though charges are usually built on a tiered schedule with the lower percentage of fees attached to the higher asset levels.

Hourly: Special project or consulting rates for advisers are often charged by the hour and can range anywhere from $100 to upwards of $300 an hour, according to a report from AdvisoryHQ.

Fixed fees: After consulting with an adviser with a fixed fee, this predetermined amount must be paid for a service, such as the creation of a financial plan. Those who charge flat fees can range anywhere from $2,000 to $7,000 a year, the NerdWallet report found.

Commission: Compensation for advisers with a commission-based fee structure charge when a purchase or a trade is made on your behalf.

Performance-based fees: Fees for performance-based compensation packages are charged when a defined benchmark is outperformed.

Advisers should have no problem talking about this, so don’t be shy when asking how they are compensated. If they are professional and abiding by the law and regulatory standards, they will be upfront with you on this topic.

6. What types of clients do you typically have?

Knowing whether or not an adviser you’re interested in working with serves clients like you may be a factor worth considering, says Bunio. “Asking what type of clients they have is important,” he says, adding that knowing whether or not an adviser “serves teachers, or those 50-plus” can help bring peace of mind that they have worked with folks in a similar financial position before.

7. Do you work with attorneys or a certified public accountant (CPA)?

If you’re a business owner and have more intricate financial planning needs, finding an adviser who works directly with an attorney or a CPA — or an adviser who can recommend one — may be an important factor. Sometimes advisers will have one on their staff who can work with you through these more complex matters, or they may refer you to someone who can. All in all, Bunio says “everyone should work together and be on the same page. If not, that’s a bad sign.”

8. How will we work together?

What resources will I have to work with? Do you have an app available to view account information and monitor your portfolio? Will statements be mailed? Do you have paperless options? Will anyone else have access to my financial information? These questions and more can help determine how you and your financial adviser will ultimately do business and work together.

Asking your adviser how, and how often, you will meet is another one of the most important questions you can ask, Bunio adds. “This is huge! I would say that it’s a red flag if it’s only twice a year or less,” he says. “Your finances are complex, sometimes I meet with my clients twice in a month.”

You may also consider asking if there are ways to meet virtually if in-person meetings aren’t possible. Ensuring they are not only financially, but technologically savvy may be more important to some than others. And since the financial planning industry can have some complicated language and concepts, knowing if they offer financial education resources can be something to consider as well.

9. Who is your custodian?

Knowing where your money is held is another key question to have answered. That’s why asking an adviser who their custodian is can be such an important question.

For some background, a bank custodian is the financial institution that physically holds your stocks, bonds, or other assets, and prevents them from being lost or stolen. Some of the best ways to know if the bank, or custodian, that they use is legitimate is to research whether they are FDIC-insured (the FDIC insures bank account balances of up to $250,000).

If you’ve ever wondered, “What is digital marketing?”

Well, you’re in the right place.

As the internet becomes more ingrained in our daily lives, the importance of digital marketing has skyrocketed.

It’s not just about flashy ads or catchy slogans; it’s about establishing meaningful connections with potential customers in the digital realm.

Using precise targeting and personalized content, businesses can reach audiences like never before.

Intrigued?

Let’s begin.

What is Digital Marketing?

Digital marketing is like a megaphone for the digital age, an orchestra conductor leading a harmonious ensemble of various online marketing disciplines.

It amplifies a brand’s voice, reaching thousands, if not millions, of potential customers on their laptops, phones, and tablets.

But it’s not just about making noise.

Successful digital marketing means saying the right thing, at the right time, to the right people. It’s about being engaging and insightful, delivering value and fostering relationships.

And what about inbound marketing, you might wonder?

While it’s true that both inbound and digital marketing strive to attract a potential customer, inbound marketing is but one piece of the larger digital marketing puzzle.

Inbound marketing focuses on creating valuable content and experiences tailored to the audience, pulling them in naturally.

Whereas digital marketing encompasses inbound tactics and a plethora of other strategies like paid online ads, SEO, email marketing, and more.

Why is Digital Marketing Important?

In an era where our lives are increasingly digital, the significance of digital marketing can’t be overstated.

As the traditional marketplaces and billboard ads give way to virtual stores and targeted online campaigns, the impact and benefits of digital marketing become even more apparent…

Reach

In the vast landscape of the internet, potential customers are just a click away.

Where else can you find millions of potential customers in one place?

Probably nowhere else but the digital world.

Think of a video on YouTube that goes viral, reaching millions globally in a matter of hours — that’s the power of digital reach.

Targeting

Digital marketing takes targeting to a new level of precision.

Imagine showing your ads only to people who are interested in your products, based on their online behaviour, interests, and demographics.

For example, an eco-friendly clothing brand can target customers who show interest in sustainable fashion, ensuring its marketing budget is spent on those most likely to make a purchase.

Cost-Effective

Budget constraints are a significant consideration for many businesses, particularly small ones.

Digital marketing is more cost-effective compared to traditional marketing, allowing small businesses to stand tall among the giants.

For instance, running a social media campaign on platforms like Facebook can be far cheaper than launching a traditional marketing strategy on television or radio.

With digital marketing, you can track the success of your marketing campaign in real-time, making necessary adjustments on the go.

You can monitor which blog posts are popular, what type of email prompts a customer to make a purchase, or which social media campaign drives the most engagement, allowing you to focus resources on what works.

Engagement

Digital marketing isn’t just about selling a product or service; it’s about building a community around your brand.

Social media platforms offer a unique opportunity to engage directly with customers, fostering a community that traditional marketing cannot.

For example, a company can launch a hashtag campaign to encourage customer participation and generate buzz around a product.

By deeply understanding the significance and mechanisms of digital marketing, you can harness its full potential to enhance your business’s online presence and foster meaningful customer relationships.

There’s a whole world of opportunities in the digital realm waiting for you to seize.

8 Vital Digital Marketing Types That’ll Amplify Your Growth

Digital marketing is a vast field with many sub-disciplines.

Here are 8 types you should know about…

1. Content Marketing

Content marketing goes beyond the confines of mere sales pitches and promotions. It’s about creating a narrative around your brand, a story that resonates with your audience on an emotional level.

At its core, content marketing seeks to inform, entertain, and inspire. Imagine creating an informative blog post that helps your readers solve a problem they’ve been facing.

They not only appreciate the value you’ve provided but also begin to perceive your brand as an expert, a resource they can trust.

For example, let’s say you’re a small gardening business.

You could create blog posts about how to care for plants, tips on organic gardening, or even step-by-step guides on creating a backyard oasis.

You’re not directly selling anything in these posts, but you’re building trust and providing value, which, over time, will likely result in increased sales and customer loyalty.

2. Search Engine Optimization (SEO)

SEO is much like a digital popularity contest. But, the vote isn’t decided by mere whims; it’s all about relevance and quality. It’s not enough to pepper your content with keywords.

Your content needs to deliver value, and your website needs to provide an excellent user experience. This involves ensuring your site is mobile-friendly, secure (HTTPS), and loads quickly.

For instance, a local bakery might use SEO strategies to rank for keywords like “gluten-free bakery in [city name]” or “organic bread in [city name]”.

With good SEO, their website would appear in the top search results when potential customers search for these terms.

These high search rankings increase visibility and drive more organic traffic to the site, which could lead to increased sales and growth.

3. Social Media Marketing

At its best, social media marketing creates a dialogue, a two-way interaction that fosters a sense of community around your brand.

It’s not just about pushing content; it’s about listening and engaging with your audience, addressing their comments and concerns, celebrating their achievements, and learning from their insights.

Take the example of a clothing brand.

On a social media platform like Instagram, they could share stylish photos of their latest collection, but they could also feature real customers wearing their products, host live Q&A sessions with the designers, or run contests that encourage user-generated content.

This approach transforms customers into brand ambassadors, amplifying the brand’s reach and authenticity.

4. Email Marketing

While it might seem outdated compared to newer, flashier forms of digital marketing, email marketing remains a crucial player in the game.

Its strength lies in its personal nature and directness.

With email marketing, you’re not broadcasting a message to the masses. Instead, you’re delivering a custom message right into an individual’s inbox.

Imagine a bookstore that sends personalized reading recommendations based on a customer’s previous purchases.

Or a software company that sends helpful tips and tutorials to new users to help them get the most out of their product.

By providing targeted and valuable content, these brands are nurturing their relationships with their customers, leading to increased retention and loyalty.

5. Search Engine Marketing (SEM)

When it comes to making your digital presence felt, Search Engine Marketing, or SEM, takes a front-row seat. SEM encompasses various paid strategies designed to enhance your website’s visibility on search engines like Google.

As the name suggests, businesses only pay when a user clicks on their ad. It’s an efficient strategy because you only pay for actual results.

Another powerful strategy under SEM is Google Ads.

With this digital marketing tool, you can have your website appear on the top of the search results for chosen keywords.

Remember, SEM isn’t just about driving traffic; it’s about driving the right traffic. With effective keyword research and careful targeting, SEM can bring in users who are ready to engage with your product or service.

6. Influencer Marketing

The power of personal recommendation cannot be understated, and that’s where influencer marketing comes in.

In this digital age, influencers — popular figures on social media — act as a bridge between brands and potential customers.

Suppose you’re a business selling hiking gear.

Partnering with an outdoor enthusiast who has a large following on Instagram could help introduce your products to an audience that’s likely to be interested.

But remember, influencer marketing is more than just celebrity endorsement. It’s about authenticity and trust.

Choosing influencers who genuinely resonate with your brand and its values is paramount to the success of your digital marketing campaign.

7. Affiliate Marketing

Affiliate marketing is a mutual beneficial approach where businesses reward third-parties (affiliates) for each visitor or customer brought about by the affiliate’s marketing efforts.

Essentially, it’s digital word-of-mouth marketing that can significantly boost your reach and sales.

For example, let’s say you sell skincare products. An affiliate, maybe a beauty blogger, reviews your product and shares an affiliate link.

Every time a reader purchases your product through that link, the blogger earns a commission.

Not only does this method drive sales, but it also improves brand awareness without a large upfront investment.

The key is to partner with affiliates who have a strong connection with your target audience.

8. Video Marketing

With the soaring popularity of platforms like YouTube and TikTok, it’s evident that video content is a kingpin of the digital marketing world. Video marketing is the practice of creating and sharing engaging videos to promote a brand, its products, or services.

Think of video marketing as storytelling in motion.

Whether it’s a behind-the-scenes look at your operations, a step-by-step product tutorial, or customer testimonials, videos can provide immersive experiences that static content often can’t.

For instance, a clothing brand might showcase its summer collection through a beautifully shot video featuring models wearing the clothes in various sun-soaked locales.

Moreover, videos are great for explaining complex concepts in an easy-to-understand way.

For instance, a tech company could use animated videos to explain how their software works.

In a nutshell, video marketing can be a creative, engaging, and highly shareable way to connect with your audience. Not only does it improve conversion rates, but it also boosts social shares, driving more traffic to your website.

Take Action by Answering What is Digital Marketing to You?

So, you’ve come a long way, haven’t you?

Maybe you felt overwhelmed at first — like stepping into a whole new world.

But here you are now, understanding the ropes of digital marketing.

It’s a brave new digital world out there, and you’re more ready than you think to conquer it.

Stand tall, knowing you’re equipped to navigate the digital marketing landscape with ease.

And remember, the digital realm waits for no one, so go forth and make your mark!

Sam is an Associate Editor for Smart Blogger and family man who loves to write. When he’s not goofing around with his kids, he’s honing his craft to provide lasting value to anyone who cares to listen.

It’s been almost six months since OpenAI dropped the ChatGPT bomb and effectively reinvigorated AI adoption across a multitude of verticals, sectors, industries and users. For the first time in years, we are seeing a large-scale commercial adoption of generative AI technology—and new applications of LLMO models are introduced by the day.

While individual uses have comprised some of the most common examples of how AI has been transforming our day-to-day workflows, the enterprise-level application of the technology is relatively overlooked, even though it holds immense potential.

Due to transformative strides on an individual consumer level, AU holds immense promise on an enterprise growth and process level—from enhancing creativity and productivity to streamlining business processes and decision making, generative AI can reform how organizations operate today.

In this article, I will explore five potential generative AI use cases for the enterprise sector which stand to unlock new opportunities and help drive innovation.

1. Creative Innovation And Branding

Generative AI opens new doors for enterprises to reach new levels of creativity and innovation—from branding and marketing efforts to content creation and internal communication or data visualization. With the help of such tools as MidJourney, Stable Diffusion, Dall-E and ChatGPT, among others, companies can produce a high-quality and high volume of content, both visual and textual.

Leaders should seek solutions that allow the brand to push boundaries when it comes to branding, brand storytelling, content creation (photo, video, text), A/B testing, blog writing, headline generation and a variety of other assets that can help push the boundaries of any brand’s online and offline presence.

Generative AI is also a powerful lever to pull for user feedback, persona development, value proposition exploration and developing customized marketing campaigns and experiences that stem directly from customer needs and asks.

2. Decisions And Predictions Based Upon Deeper Foresight

Forecasting, future-proofing and planning are the cornerstones of successful enterprise management. In other words, leaders must constantly strive for efficient and sustainable growth built upon data-driven and well-informed decision making.

Generative AI offers a significant boost in this area by providing organizations with advanced data analysis and predictive analytics capabilities. By analysing large volumes of structured and unstructured data, generative AI can provide immediate and accurate insights, aiding decision makers in formulating strategies, optimizing processes and predicting industry trends.

Generative AI isn’t just a powerful source of predictive analytics. Its progressive capabilities also include simulations of potential scenarios if provided with all variables to account for—which creates a clear scenario to aid in data-driven decision making, risk mitigation and opportunity discovery.

3. Streamlined Workflows, Operations And Processes

Generative AI’s ability to analyse data and identify patterns stands as a powerful solution for optimizing workflows, identifying inefficiencies and building processes that are significantly more streamlined and automated. The application of this includes but is not limited to supply chain management, resource allocation and workflow automation—with generative AI transforming labour-intensive tasks into efficient and accurate processes.

In other words, generative AI is also able to assume more administrative or time-consuming, repetitive tasks that would otherwise prove to be a waste of time for employees who strive to drive more impact and plan strategically on a managerial level. This can not only save time and reduce costs but also enhance overall productivity, enabling employees to focus on more strategic and value-driven/high-involvement activities.

4. Personalized Customer Experiences

Building on the major branding, storytelling and marketing benefits of generative AI, the technology also opens doors to new ways of delivering exceptional customer experiences. Generative AI provides brands and organizations with the tools to personalize their interactions with customers on a whole new level—from more powerful chatbots that proactively react to the customer needs to providing unique personalized recommendations to customers based on their preferences and previous activity.

By analysing large amounts of customer data, generative AI can generate individualized product/service recommendations, highly targeted ads and customized user interfaces fit for every user’s personal activity patterns. This is a direct path to higher customer satisfaction, loyalty and engagement while ensuring higher consistency in conversions and bottom-line impact.

5. Accelerated Research And Development

Research and development (R&D) is largely where innovation happens within the enterprise sector. Improving this sector is like throwing a brand new lifeline to any enterprise business—and generative AI has the power to significantly accelerate the R&D process by assisting in the ideation, prototyping and testing phases.

The simulation capabilities generative AI offers can allow for the mapping and exploration of a variety of formulas, outcomes, products and prototypes while significantly shortening time to market and product launches. This can allow businesses to stay ahead of the competition, adapt to rapidly changing markets and deliver cutting-edge solutions to their customers.

Revolution In The Enterprise Sector

Generative AI holds tremendous potential to provide organizations with unprecedented capabilities to innovate, streamline internal and external workflows and deliver custom-tailored experiences to their customers. From empowering creative positioning and branding initiatives to improving data-backed decision making, generative AI holds the potential to drive enterprise to new heights of success.

As the enterprise sector continues to adopt generative AI, leaders must build out strategic initiatives that invest in the necessary infrastructure, talent and resources to remain ahead of the curve and leverage the technology in full capacity. Close partnerships with AI experts, data scientists and researchers are only one of the many ways to efficiently incorporate generative AI into existing business processes and systems.

Gary Fowler is a serial AI entrepreneur with numerous startups and an IPO. He is CEO and cofounder of GSDVS.com and Yva.ai. Read Gary Fowler’s full executive profile here.

The DEI Census Report provides a comprehensive analysis of the global industry’s performance across a wide range of metrics related to diversity, equity, and inclusion (DEI). It is a significant undertaking that explores various protected characteristics, including race, national or ethnic origin, colour, religion, age, gender identity or expression, family status, and disability. Furthermore, the report examines aspects such as positions, salary, and, most importantly, the lived experiences of individuals within the industry.

The Marketing Institute’s Breakfast Series is a highly regarded professional development event that brings together marketing professionals, industry leaders, and experts to discuss the latest trends, insights, and strategies in the dynamic field of marketing.

Dates

September 21st, October 19th, December 7th, January 18th, February 15th, April 18th, June 20th.

We are thrilled to announce our exclusive member only events activity. Stay tuned and keep an eye on your inbox for forthcoming announcements. We are working diligently to bring you unforgettable experiences designed exclusively for our valued members.

August 16th: Diversity Attitudes – How inclusive are we?

Travel bargain hunters are a fickle bunch, visiting more than two dozen websites on average before they book. Booking.com and its rivals spend billions annually to woo those travellers who wouldn’t otherwise click over to their platforms.

Online travel is a weird industry when it comes to its outsized marketing spend as compared with other types of businesses.

None of this is shocking because it’s been the pattern for many years, but a BTIG investor report published Thursday put Booking Holdings’ marketing spend in a different context.

Booking Holdings, which owns brands including Booking.com, Kayak and Priceline, spent around $6 billion on marketing in 2022 — and that was about 35% of its total revenue. BTIG stated that Booking gets around 50% of its traffic direct; around 20 percent from free search engine listings; roughly 15% from social media, email, display ads and referrals, and 15% from paid search engine marketing — “and it spends billions annually to get that last piece.”

That’s worth repeating: Booking Holdings spent around $6 billion on sales and marketing last year to attract just 15% of visitors to its platform. (Sure, it directs some of that spend toward goals other than luring travellers to its platforms, but you get the general idea.)

How Expedia and Airbnb Do It

Over at rival Expedia Group, its marketing spend was even more top-heavy — around 47% of revenue last year.

Airbnb is an outlier in the online travel agency space because around 90% of its customers come directly to its website or app, as well as from free listings in search engines. You’ve heard the company’s talking points ad infinitum: Airbnb is so mainstream that it’s “a noun and a verb.”

So Airbnb focuses on limiting its paid search engine marketing on platforms like Google and Bing. Airbnb shelled out a very modest 18% of revenue on marketing in 2022.

Yes, before the hate mail arrives, it’s true that the three companies calculate marketing spend differently, but the basic points about their marketing spend as a portion of overall revenue hold true.

Airbnb Smart, Booking Foolhardy?

All of this is a contrast to most U.S. industries, according to a 2022 Gartner survey, which found them planning to spend a relatively minuscule 6-10% on marketing as a percent of revenue last year.

But before you leap to the conclusion that Booking’s strategy (35% of revenue on marketing) is dumb, and Airbnb’s approach (just 18%) is valedictorian-worthy, consider that Booking’s profit margin was considerably higher than Airbnb’s or Expedia’s last year.

Booking’s 2022 EBITDA margin was 31.3% compared with 23.2% for Airbnb, and 11.9% for Expedia. (True, their businesses are different as they sell some different things, and they are spread out across different geographies.)

Booking “has historically had an advantage in paid channels with a higher conversion rate, allowing it to bid more efficiently,” the BTIG report stated.

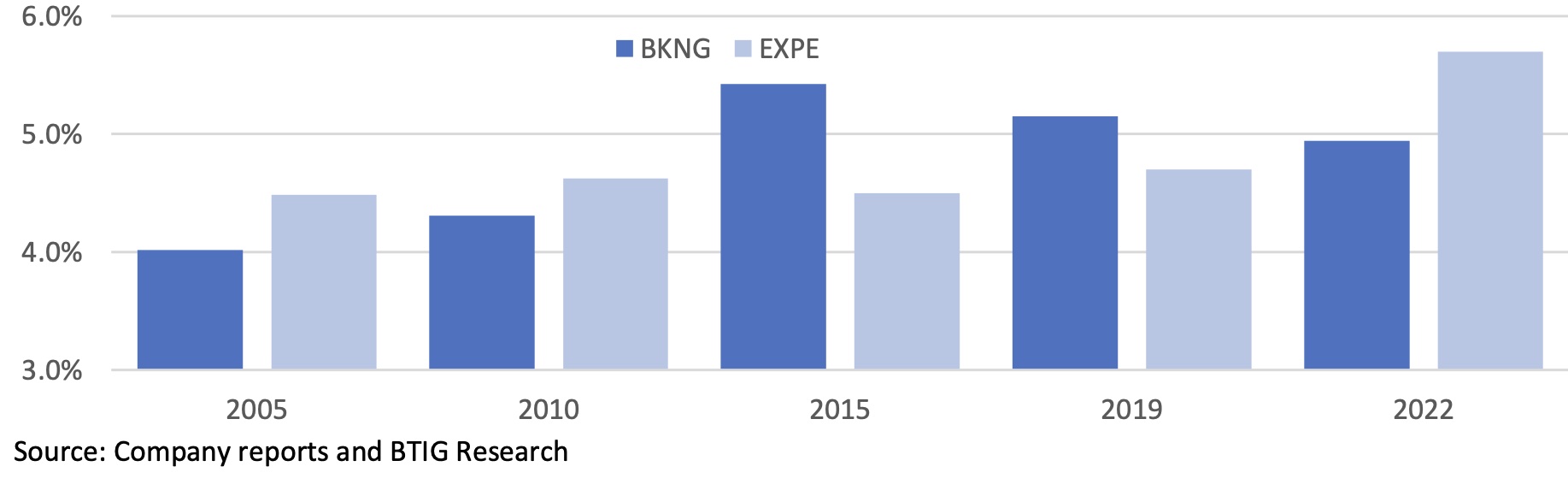

Another way to look at Booking’s advantage over Expedia is in marketing spend as a percent of bookings, not revenue, and by this metric Booking was more efficient, 4.9% versus 5.7%, according to BTIG.

Marketing as a Percent of Bookings, Booking Versus Expedia

Regarding these companies’ big-stakes marketing programs, now you know how strategic it is for them to try to attract more free, direct traffic to their websites and to coax more app downloads. It’s all in the hope that their customers won’t stray once they land on their websites, and won’t have to be enticed with billions of marketing dollars all over again.

Unlock the secrets to optimising your ad spend and driving business growth

Starting a new business can be an exciting journey, but it also comes with its fair share of challenges. One crucial aspect of any start-up’s success is the effective allocation of the advertising budget. As a start-up, you might have limited resources, making it vital to make every penny count when it comes to promoting your products or services.

Here’s a guide on how to allocate your start-up’s advertising budget effectively,

In today’s competitive business landscape, simply having a great product or service is not enough. You need to make sure your target audience is aware of your offerings and compelled to choose your start-up over the competition. This is where a well-thought-out advertising strategy plays a pivotal role. By allocating your advertising budget effectively, you can reach your target market, drive brand awareness, and generate valuable leads.

Set clear goals and objectives

Before diving into advertising channels and budget allocation, it’s crucial to set clear goals and objectives for your marketing efforts. What do you aim to achieve with your advertising campaigns?

Is it to increase brand awareness, drive website traffic, generate leads, or boost sales? Defining your objectives helps you align your advertising budget with your business goals. Additionally, understanding your target audience and their preferences is essential in crafting effective advertising messages.

To allocate your budget effectively, you need to research and analyse various advertising channels available to your start-up. Each channel has its unique characteristics and audience reach. Start by evaluating traditional advertising channels such as print media, television, radio, and outdoor billboards. Consider the cost, reach, and effectiveness of these channels based on your target audience demographics and psychographics.

Simultaneously, explore the opportunities offered by digital advertising. Digital channels, including social media platforms, search engine marketing (SEM), display advertising, and email marketing, provide targeted and cost-effective options for start-ups. Analyse the behaviour and preferences of your target audience to determine which digital channels resonate with them the most.

Determine budget allocation percentages

Once you have researched and identified potential advertising channels, it’s time to determine the budget allocation percentages. Start by setting a realistic overall advertising budget based on your start-up’s financial capabilities. As a general rule of thumb, allocate a percentage of your projected revenue or a fixed amount suitable for your industry. Next, consider the effectiveness and reach of each advertising channel. Allocate a higher percentage of your budget to channels that have a proven track record of generating results and reaching your target audience effectively. Keep in mind that budget allocation should be dynamic, and it’s essential to monitor the performance of different channels regularly and make adjustments as necessary.

Embrace digital advertising

In today’s digital age, digital advertising has become a crucial component of effective budget allocation. Digital channels provide extensive targeting options, allowing you to reach specific demographics, interests, and behaviours. Social media advertising offers advanced targeting capabilities, allowing you to tailor your ads to your audience’s preferences and maximize relevance.

Search engine marketing (SEM) is another powerful digital advertising tool that ensures your start-up appears prominently in search engine results for relevant keywords. By embracing digital advertising, you can leverage the vast reach and targeting options available, reaching your audience where they spend a significant portion of their time—online.

Here’s why launching a digital PR campaign won’t make sense until you’ve established a solid and consistent digital strategy.

As a head of a PR agency, I’m often reached out to by brands asking me to launch a full-scale digital PR campaign. Rather unexpectedly for them, sometimes I decline or suggest they push their plans back a bit.

The reason is that I firmly believe PR won’t make sense if a brand hasn’t established a solid digital strategy. Getting featured in some top-tier media is nice, but it won’t necessarily result in many new leads, increased online visibility and skyrocketing revenue. Top-tier publications alone won’t bring you clients or brand awareness, especially for brands that hardly have any digital presence.

Imagine you’ve got a car and want to level it up and tune it. Ah, the neon lights and shiny car rims. Are you good to go? Maybe. Only if you are certain that all the rest performs well. Gear unit, engine, headlights — are you sure these work fine? PR is the tuning that you make while ignoring all the rest.

The “Featured in top-tier media” bar on your website is good, but it won’t matter if this is not part of your consistent digital presence strategy.

Think long-term, and align efforts with other teams

Including PR in the long-term digital marketing strategy is the number one thing I recommend to the brands. Pavel Katz, CEO of growth marketing agency Digital Bands, also emphasizes the importance of having a content strategy that covers all digital channels and making sure PR publications are aligned with it: “Outline a very particular content plan with specific dates and leave some place for the unscheduled posts and announcements. Press releases and planned publications should be reflected in it too. I know this sounds like quite a lot of work for several teams, but this will take your digital marketing efforts to the next level.”

Things only start here. After the content strategy is ready, there are a number of other steps that will help brands enhance PR efforts.

Talk to sales. Talk to marketing. Talk to SEO and business development teams. Your digital presence might diverge unless your efforts align with the other departments. Tip: Schedule a call with a sales/business development lead, and ask them to help you map a buying persona. That’ll help you know [rather than guess] who your target audience is. Even if you do B2B, there’s always a particular person behind this “B” who will decide whether to cooperate with you. Know the pains of this person, address them, talk to them, and help make a well-informed decision through PR.

Level up your socials

Along with the PR publications, social media is your brand’s front face, which clients and other stakeholders judge you upon. Ensure your online reputation strategy syncs with the PR and social media teams. Hints: Agree on the tone of voice, discuss crisis management steps in advance, and discuss what kind of brand image you broadcast through socials and PR efforts.

Don’t forget to show your PR publications to your social media audience. You can launch a paid social campaign that showcases the PR mentions and target a particular audience that you’d like to see your posts. It allows you to increase your PR reach and tweak the ad displays as per your targets. For example, you can show Facebook ads with a PR mention to people who submitted requests on your website. It also doubles as a solution to an eternal PR metrics problem: You can track how many people have seen and engaged with your publication through such ads.

For instance, after my previous article was featured in Entrepreneur, I posted a link to it on my LinkedIn along with a catchy intro that encourages my connections to read the entire post (you can do better than “I was featured in /media/, read the entire piece here,” but most intros do boil down to that). Journalists appreciate when their pieces are placed on social media and get additional coverage. I noticed it got decent traction and engagement from my colleagues and friends, so I launched a small-scale paid social ads campaign on LinkedIn, which gave my post a proper boost. It’s a win-win for me and the media: The article is seen more often, gets more hits, and I can track down how many people saw my feature.

Technicalities and HyPRlinks

Audit and fix your website. That’s an art in itself, but leveraging Google Analytics is a good start. This way, you can identify how your website performs and what can be improved. Example: We had a client whose website sucked when it came to its technical performance; it just didn’t load quickly enough. All the hreflangs, XMLs, javascripts and other front- and back-end incantations might damage your website performance and hence hurdle PR. No one wants to deal with trudging through sloppy pages.

Digital PR implies media linking to your website; thus, exploring your current backlink profile makes sense. You need to know which websites have already linked to you to gain momentum by securing new links. Often, links from niche websites will get you more reach than from top media.

You can use SEO tools for both technical website audit and backlink profile exploration. These may seem tricky, but as I advised earlier, you’ve talked to the SEO team, right? PR + SEO is a secret weapon neglected by 9 out of 10 PR specialists I speak to, so be among the few who use it.

Take your time

As I mentioned in the beginning, I often advise my clients not to start the PR campaign right away. After all, the odds are they won’t even need PR at their current stage, and it’s fine. Sometimes we prefer to ramp up our efforts gradually, and the first steps can be pretty straightforward. Linking back to your website in your YouTube video descriptions is PR, too. Asking a partner you’ve cooperated with to announce your cooperation on their social media also matters.

It’ll be much easier to gain traction in the media you want to be featured in if your overall digital presence is solid and your brand’s digital efforts are aligned. There are no details that won’t matter. Before you make it to the main page of the media you dream about, you’ve got to do your digital homework.

Entrepreneur Leadership Network Contributor. Evgeniya Zaslavskaya is the founder and CEO of ZECOMMS AGENCY, a communications agency that provides PR services for companies and startups in the field of IT and investment in the regions: North America, Europe, Latin America, Middle East and Southeast Asia.

‘Just Do it’ is one of the best-known brand taglines around. It’s been serving Nike since 1988, and it’s just as recognisable as its swoosh logo, one of the most famous textless logos. Many would say it didn’t need any other intervention, which has left people perplexed as to why Nike appears to have jumped on a recent typography trend.

People have been commenting on social media to ask why the brand placed a couple of apparently random gothic Blackadder-style letters on a post featuring Spanish tennis star and current men’s singles number one Carlos Alcaraz. But it’s not the one advert. Nike has been changing up the ‘D’ in several recent adverts.

Adaptive logos are having a bit of a moment right now. It’s something that MTV logo did so well back in the 1980s, and the LA28 Olympic Games logo has resurrected the concept with a design that can take on infinite interventions, including, controversially, from the games’ sponsors.

Nike appears to be taking up this idea and running with it, not on its logo, but with the ‘D’ in its ‘Just Do it’ tagline. But people are confused (and not just because of the incorrect punctuation). “What’s with the random Blackletter E and D? Totally unnecessary and adds nothing,” Studio Koto CEO and founder James Greenfield commented on Twitter about the recent advert featuring Alcaraz. Some people even wondered if the design was a real Nike advert or an amateur proposal.

")