For years, local businesses have relied on visibility metrics to measure marketing performance. Rankings, reviews, profile views, and website traffic became the standard indicators of success because they appeared to correlate with customer acquisition.

As a result, many business owners came to believe that higher rankings automatically meant more business.

After reviewing businesses across roofing, plumbing, HVAC, electrical services, and legal services, I noticed a consistent pattern. Many had strong rankings, growing reviews, and healthy Google Business Profiles, yet phone calls were not increasing at the same pace. Some were receiving fewer inquiries than they had several years earlier despite improved visibility.

But the more businesses I looked at, the less those explanations made sense. Instead, I started to wonder whether the real problem was that businesses were still measuring success using a model that no longer reflects how Google works today.

The Original Customer Acquisition Model

For years, the formula was simple. Rank higher on Google, get seen by more people, and generate more leads. In many cases, that’s exactly what happened.

Businesses focused on local SEO because improvements in visibility often translated directly into more calls and customer inquiries.

Back then, most customers followed a similar path.

Since businesses could see this journey happening, higher rankings usually translated into more website visits, more calls, and more leads. That’s why most marketing reports focus heavily on visibility metrics.

The challenge is that the way people use Google today is very different from the way they used it when most local SEO reporting models were developed.

Google’s Incentives Have Changed

Local businesses want one thing: more customers. Whether that means more calls, more appointments, or more revenue, the goal is the same. Google’s goal, however, is not exactly the same as the business owner’s.

Google’s goal is simple: help users complete tasks as quickly as possible. The fewer clicks required, the better the experience. That’s why Google increasingly provides enough information directly in search results for users to make decisions immediately.

Over time, Google has made it easier for users to complete tasks without leaving its ecosystem. We’ve already seen this happen with hotels, flights, restaurant reservations, and shopping. More decisions are happening directly inside Google’s ecosystem, and local services appear to be following the same trend.

The Rise of Action-First Search Results

Today, someone searching for a plumber may never visit a company’s website at all. They can see reviews, business hours, service details, credentials, and a call button directly on Google. In many markets, Local Service Ads appear at the very top of the page and provide enough information for a customer to choose a business and make a call immediately.

As a result, the customer journey often looks much simpler:

Search → Local Service Ad → Phone Call

The website is no longer a required step in the process. Yet many businesses still measure success using models that were built when websites played a central role in generating leads. That’s why some companies struggle to understand where their customers are actually coming from.

The Attribution Problem

Here’s a question I often ask business owners:

“Do you know exactly where your phone calls come from?”

Most know how many calls they received.

Very few know where those calls originated.

That’s because many reporting systems combine everything together. Calls from Google Business Profiles, Local Service Ads, websites, and other sources often end up in the same report.

The result is that businesses see the final number but miss the story behind it.

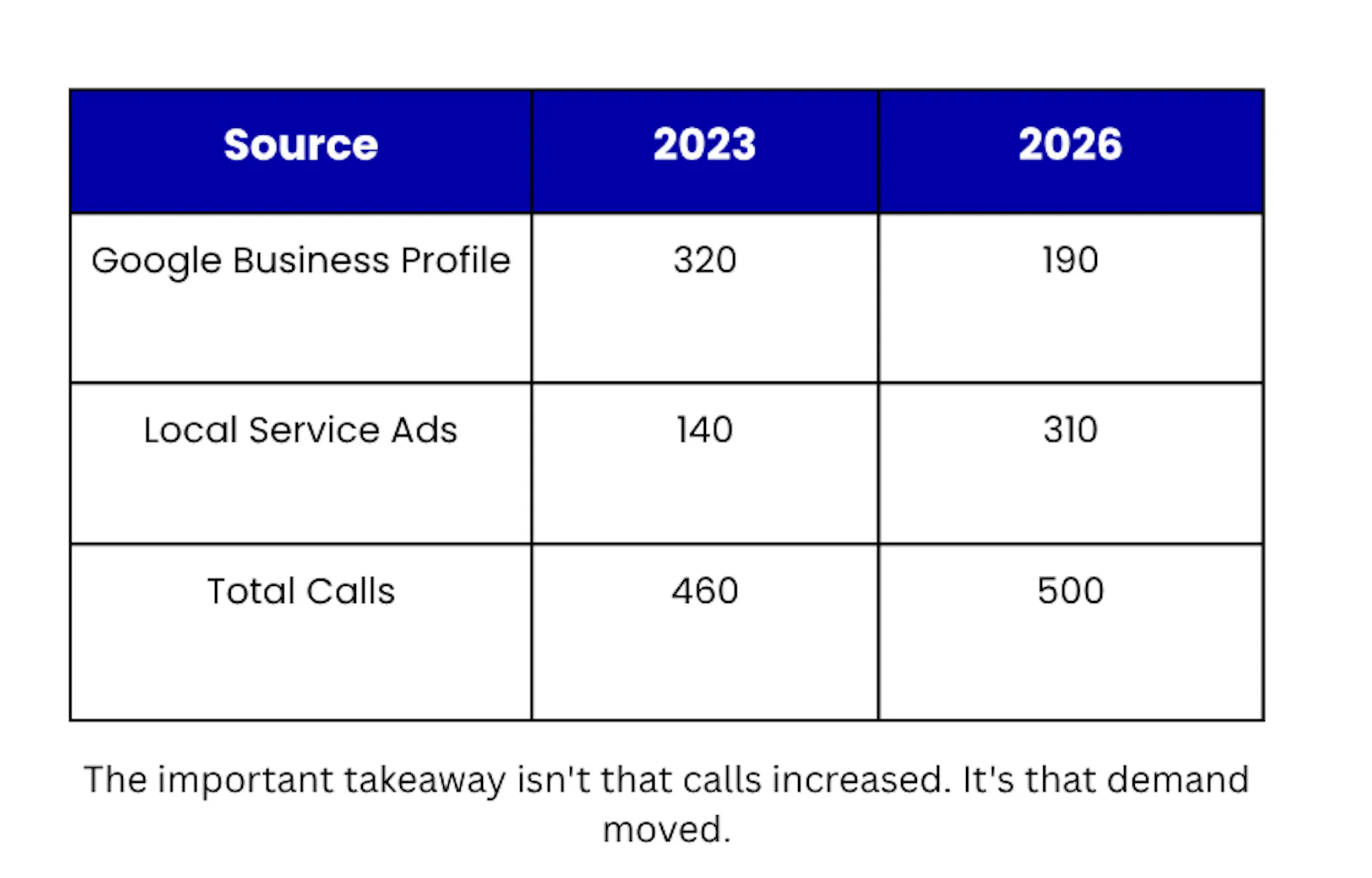

For example, consider a hypothetical plumbing company. Total call volume increases from 460 to 500 over three years. On paper, that looks like growth.

However, the source of those calls changed dramatically. Google Business Profile calls fell by more than 40%, while Local Service Ads became the dominant source of demand.**

The lesson isn’t that calls increased. It’s that customer behaviour has changed. Without source-level attribution, the business would likely continue focusing on rankings and visibility metrics without realizing how customers were actually finding them.

Google Quietly Created Two Customer Acquisition Systems

I think one mistake many businesses make is assuming they’re competing in a single Google system.

In reality, there seem to be two different systems at work.

The first is traditional local SEO. This is where factors like proximity, relevance, reviews, business profile optimization, and website content help determine visibility in local search results.

The second is Local Service Ads.

LSAs appear to care about a different set of signals, such as how quickly you respond to leads, whether calls are answered, your availability, booking activity, review growth, and the quality of customer interactions.

A business can rank extremely well in local search but struggle to generate leads from LSAs. At the same time, another business with average local rankings can generate a large number of calls through Local Service Ads.

If you treat both systems the same way, you may end up optimizing for the wrong things.

Visibility No Longer Guarantees Demand

To be clear, I’m not saying rankings don’t matter.

Visibility is still important.

If people can’t find your business, they can’t contact you.

But rankings only tell part of the story.

Many businesses assume that better rankings automatically lead to better results. That’s not always true anymore. A company can dominate local search results and still struggle to generate calls if it’s focused on the wrong channel.

The businesses seeing the best results today are usually the ones paying attention to customer behaviour, not just rankings.

The larger issue is that many businesses are still measuring local search using assumptions that were formed when websites sat at the centre of the customer journey. As Google reduces the distance between discovery and action, those assumptions become less reliable.

The Future of Local Search Measurement

As Google makes it easier for people to take action directly from search results, knowing where your leads come from will become more important than ever.

Businesses will need to separate calls by source to understand what’s actually driving growth.

This doesn’t mean local SEO is going away. Strong rankings, positive reviews, and an optimized Google Business Profile will continue to matter.

What’s changing is how those factors turn into customers.

The businesses that succeed over the next few years won’t just be the ones with the best rankings. They’ll be the ones who understand where their customers are coming from and which channels are generating real revenue.

In this op-ed, Phil Ohren, CEO & co-founder of Intender highlights the move of GPT ads going from being an industry rumour to a market reality. He believes if your first question is ‘What keywords should we target?’, you’re asking the wrong question.

ChatGPT has officially entered the media mix.

OpenAI’s Ads Manager Beta now includes campaign creation, billing, access management and reporting, with advertisers able to run campaigns in Australia, New Zealand, Canada and the US. Ads are also now appearing for ChatGPT Free and Go users in Australia and New Zealand.

The predictable response will be to ask the same question the industry asked when search advertising emerged: What keywords should we target?

But that’s the wrong question.

GPT Ads are not built around keywords. They are built around conversations. People use AI to ask for help, explore problems and seek advice before they know exactly what product, service or category they need.

The brands that win will not be the ones that target what people say. They’ll be the ones that understand what people mean.

People do not talk to AI in keywords

A family looking for a seven-seat SUV may never mention SUVs.

Instead, they might say: “Our third child is on the way and suddenly nothing fits in the car.”

Or: “Every weekend we need two cars because we can’t fit the kids, the dog and all the gear.”

Same intent. Different language.

For two decades, digital advertising has been built around signals like search terms, audience segments and browsing behaviour. Those signals still matter, but AI introduces something more powerful: context.

People don’t interact with AI using keywords. They describe circumstances, frustrations and goals.

The commercial opportunity often emerges before the obvious keyword appears.

A bank should think beyond “home loan” to the couple wondering whether rent is rising faster than their ability to save for a deposit.

An insurance brand should think beyond “life insurance” to the new parent suddenly feeling responsible for someone else’s future.

A B2B software company should think beyond “CRM platform” to the sales leader realising their pipeline forecast is fiction.

In each case, the signal exists before the search.

The new media unit is the moment

If GPT Ads scale, the winners will be the brands that understand real-world context better than their competitors.

A customer moment might be a homeowner comparing renovation options before requesting quotes, a marketing leader trying to understand why performance has stalled, a consumer deciding which financial provider they can trust.

These moments matter because they sit before the transaction. They are where people define the problem, compare options and decide who feels credible.

That’s why GPT Ads should not be treated as a small experimental item on the media plan, but prompt marketers to ask a bigger question:

Where are our customers asking for help before they make a decision?

What marketers should do next

First, stop briefing GPT Ads like search campaigns. Start with customer context, not keywords.

Ask:

What situation makes our product or service relevant?

What would a customer ask before they need us?

How can our brand be genuinely useful in that moment?

Second, bring teams together earlier.

Paid media, SEO, content, brand and conversion teams need a shared understanding of the customer. In an AI environment, people don’t care which department

owns the answer – they just want help.

Third, measure quality, not just volume. Don’t just ask whether GPT Ads drive clicks. Ask whether they drive more informed prospects, stronger engagement and higher-quality demand.

Context will expose weak strategy

This is where some brands will struggle. Many organisations still operate with different teams working from different assumptions about the customer. In a conversational environment, those disconnects become obvious.

The ad, content, landing page and follow-up experience all need to reflect the same customer reality.

Generic copy won’t cut it. Neither will a keyword list dressed up as an AI strategy.

The brands that succeed will understand the situation behind the query – what customers are trying to solve, what concerns they have and what information they need next.

The future belongs to brands that understand meaning

The first wave of GPT Ads will probably resemble the early days of search: broad targeting, recycled copy and campaigns built around obvious keywords.

That won’t last. GPT Ads are not just a new channel. They’re a signal of where advertising is heading: towards context, intent and usefulness.

By all means, test GPT Ads. But test them properly.

Start with the customer moment. Build around the situation. Connect the message, content and

landing experience.

Because the future of advertising won’t belong to the brands that simply target what people say.

It will belong to the brands that understand what people mean.

And yes, AI is a factor. Replika and Wabi founder Eugenia Kuyda on how advances in coding changed her hiring calculus

This is an interview about AI. My fiancé works at Anthropic. See my full ethics disclosure here.

Last week in our series on AI and jobs, Brookings’ Molly Kinder warned us to prepare for a “messy middle”: a long, “politically explosive” stretch in which AI job losses are concentrated among some of the best-paid workers in the economy. This week, for the first-ever Platformer live show, I wanted to talk to someone who believes in that vision: a founder building the tools that might bring it about, and who turned out to be unusually candid about what that might cost us.

I’ve known Eugenia Kuyda for more than a decade. In 2015, after her best friend Roman Mazurenko died in a car accident, she gathered the text messages he had sent to friends and family and built a chatbot that let them speak with him again — a story I covered at the time for The Verge, nearly a decade before ChatGPT made chatbots ubiquitous. That project was the seed for Replika, the AI companion app that now claims more than 40 million users. Kuyda’s latest startup, Wabi, takes AI in a different direction — away from personal entertainment and into the world of work. The app, which is now available for iOS, lets you vibe-code apps on your phone using text prompts. Over the next year, Kuyda hopes to shift more of the team’s work away from standard enterprise software toward apps built on her own platform.

Kuyda argues that we are living in “the Microsoft DOS era of AI interfaces,” and that we’re desperately in need of a Windows equivalent: an easy-to-use graphical user interface that lets the average person take full advantage of agents and personalized software. When that happens, she predicts, the long tail of subscription-based apps — the calorie counters, meditation apps, and fitness trackers of the world — will start to disappear, replaced by software that we make and share ourselves.

But what struck me most during our conversation was her answer to the question at the heart of our podcast miniseries. When we began, I expected that more tech executives would tell me they expect AI to cause job loss. Instead, it’s been the opposite — most of them have said that advances in AI will only increase demand for software engineers and other knowledge workers.

Kuyda is our first guest to say plainly that she believes that is a fantasy. The fear of job loss is “super justified,” she told me; in her view, AI has made hiring junior employees “extremely expensive and completely unsustainable for a startup,” because every hire now competes with the leverage of what she calls a “1,000x engineer.” “I think the crazy protests around jobs and AI are going to start happening,” she said. “We live in this very optimistic city, where it’s all about future, future, future — but as soon as you get out of here, it’s pretty scary.”

She’s building Wabi accordingly: the company is modelled on a soccer team, she told me, with 10 to 15 superstar “players on the pitch” who get sizable equity and public-facing roles, supported by contractors in the back office. She doesn’t think you need more than that to build a billion-dollar company anymore.

Whether that turns out to be true depends in part on Kuyda’s own bet on Wabi. Can vibe-coded apps truly compete with enterprise software in the way that she hopes? Or will most companies continue to prefer the stability and support that comes with traditional software as a service?

We should get more data on that point soon: Kuyda told me on the show that after a year in beta, Wabi will launch publicly before the end of the month.

Highlights of our conversation are below, edited for clarity and length. Listen to the entire conversation wherever you get your podcasts — just search for Platformer — or watch it on YouTube at youtube.com/caseynewton.

And let us know what you think — we’re new to podcast production, and welcome your feedback at [email protected].

Casey Newton:So it’s 2015. You are almost a decade away from ChatGPT. What were you seeing that made you think, “I can actually use the tools that are here to make a kind of prototypical chatbot, and that will be an interesting thing to explore”?

Eugenia Kuyda: We actually started a company that was building chatbot tech in 2013. What kick-started that was a friend of mine who used to work at Google DeepMind showed me this technology called word2vec, which was the original tech to basically transform language into math — to let computers understand words, in a way. ImageNet also dropped, and I was like, whoa — soon that will somehow come together, and we’ll have these new neural networks that will understand language. I used to be a journalist before that, and we had this gigantic sign in neon: “The limits of my language are the limits of my world.”

Newton:Which is a Wittgenstein quote, if I remember right.

Kuyda:I felt like if we figured out how to build language models, that would probably be the closest to understanding the world as well.

So we started building that, way before any of the first language models. Then in 2015, Google published a paper where they talked about the first deep learning model applied to dialogue generation, and we decided to hire every possible NLP researcher we could find to focus on these language models. And then, of course, after Roman passed away, we built that AI for him. We were struggling to find a consumer application, and that was it. We were like: maybe we can’t yet build a chatbot that talks eloquently with people and has meaningful conversations, but maybe we can build one that can listen, and that would probably be enough for many people out there.

Newton:How confident were you when you were doing that?

Kuyda: We thought it would work at some point. The models were so crappy in 2016, when we started Replika, that they would just produce non sequiturs. These were sequence-to-sequence models, and of course there were no models off the shelf or through APIs, so we had to build our own — this was right before people moved on to transformers. So it was very hard to say, “Okay, this will become what it is today.” We just felt that it would happen; we didn’t know when. For us it was more like: okay, maybe the tech is lagging, but it’s less about tech capabilities — it’s going to be more about human vulnerabilities. There were so many people who wanted so much to have some connection — someone to listen, someone to hear them out, to accept them, to understand them — that maybe in the beginning just those people would react positively to it, and as the tech got better, we could increase the range of people it would resonate with.

Casey: I think there’s something really poignant about the fact that even though the technology, by today’s standards, was maybe not that good, the human desire and need for support and connection was so powerful that people looked right past it. But at the same time, I wouldn’t downplay the technology either, because when I was talking with Roman’s friends and family, the part of the story that will still make me cry when I tell other people about it is how much people learned about their friend and family member after he passed away, and how their relationship with him changed after he passed away, because of the conversations they were having in this app. That was honestly the moment when I started to take AI more seriously, because I thought: if people can feel that deeply even in this very primitive version of the thing that we have today, there just has to be something there.

Kuyda: I think so. And looking at my previous relationships — oftentimes we do have relationships with people where maybe they don’t respond that much, or it’s more about our fantasies. How much do we put in? A good example is talking to God. So many people talk to God, and maybe he doesn’t really respond.

Newton:He’s sort of famous for leaving you on read.

Eugenia: I also had a lot of experience going on dates where you just listen, and maybe ask, “Oh, tell me more,” and then the guy would be like, “Oh, that was the best conversation I’ve ever had.” And you space out half the time when they’re talking — you’re thinking about all the groceries you need to buy. So I’m like, if this is the level of understanding that’s required for the most amazing conversation, we can probably build that.

Casey:Once you realized how low the bar was, you thought, “There’s a unicorn here.”

I want to zoom out and ask you a question about your two companies, because on the surface they look quite different, right? One is about an AI that you develop relationships with; the other is a tool for making apps. In your mind, are they completely different, or do you see a through line there that you’re chasing?

Eugenia: They’re definitely different things, but for me the idea was always: how can we make a person’s life better, or help them unlock their potential? With Replika it’s easy — it was always about building an AI to help people flourish and feel better in the long term. We had some big studies published around that with Stanford and Harvard, some of them published in Nature, where we proved we were doing that.

With Wabi, the idea is: most of our time today is spent on our phones, using software that’s not built by us — built, in David Foster Wallace’s words, by people that don’t love us, that want us to just scroll or click on things. We shape our buildings, and then they shape us. It’s the same with software — we shape our software, and then it shapes us. Only we don’t shape it; someone else does.

So in this new era, where anyone can really build something in a matter of a few seconds, why not let people take a little bit more agency? Maybe not build every app they use, but at least have software be more decoupled from this model where every app needs to be a business. Wabi is a platform where people can make apps, but can also discover, remix, and use them with their friends and their families. It’s a social platform where you can quickly spin up any app, or find any app, and start using it with whoever you want. In my case, that means creating software that really fits my life — whether it’s helping me learn more about the art movements I’m into, or the language I forgot, or teaching my kids something, or finding cool events to take my kids to, or even just a better weightlifting tracker.

Casey: What is a feature or a design element of something you’ve built that made you feel like, “This is truly, personally for me — I would not expect to encounter this kind of app anywhere else”?

Eugenia: When you take away the idea that you have to make an app, put it on the App Store, distribute it, and make it for some audience, it can just be n-of-one. For me, I have an app that teaches me a daily philosophy concept.

But that’s the simple way of putting it. The more interesting reason I really decided to work on this is that I do believe we’re in the Microsoft DOS era of AI interfaces, where everything’s a chatbot. I’ve worked for 10 years on a chatbot, and I do believe there will be a GUI moment — a Windows, macOS moment — that will come to AI. Mostly because even though the model capabilities became so much better over the years, most people — normies, I guess, us included — still use ChatGPT and Claude mostly the same way they used them in 2022 and 2023: ask questions, search, do homework. That’s it. It’s not all these crazy agents — they’re not spinning up cron jobs or figuring out Claude Cowork, even. And really, that’s because through text, through a chatbot, it’s very hard to discover anything.

Casey:It feels like talking to the Alexa in your house, right? It can set a timer, and it can check the weather, and it can do 1,000 things, and you don’t know what those things are — so you just use it to check the weather and set a timer.

Eugenia: Exactly. But even if you set a timer, you need to see that timer. Chat is great as one of the interfaces; it cannot be the primary one. People love to tap, tap, tap, click, click, click, scroll, scroll, scroll. And that’s the only way to really make things discoverable and multiplayer.

Casey: Talk about the demand that you’ve seen for Wabi so far. Sometimes I feel like a freak, because I like to use software — I love productivity tools. Most people don’t feel that way. So talk to me about these people who are out there saying, “I need to build a philosophy app that only I will understand.”

Eugenia: It’s really just about making this tool simpler for people to use. We’re still in private beta — we’re going public in the next two weeks, so I’m super excited about that.

But I think we grow up being more creators, and at some point we become consumers. Kids use Roblox — kids make these games, kids hang out in these environments they make for themselves. And then at some point we just turn into these passive consumers: scroll, scroll, scroll, and subscribe, subscribe, subscribe. I think once you show people that it’s actually very easy to make something — or not even make something; maybe we just suggest some apps for you that someone else made, and it’s very easy to remix them. The agent says, “Hey, I see you added this app. I know all your apps are black and white — let’s change this one into black and white, too.” So it’s proactively helping you use all this software.

But I do believe software needs to change. If we’re just using AI to write the same old apps from the past, that’s pretty boring. What needs to happen is new agentic apps, where all apps have agency and are more alive. What I mean by that is that you can change them, they can suggest how you can change them, they can grow with you, they can evolve with you — and they can also talk to you. Right now, apps can only send you push notifications. With Wabi, all apps have a chat, so the push notification becomes “Time to work out” — but you can also say “Stop messaging me” as a response. You can change everything right there in the chat. Chat becomes the way for an app to talk to you, but also the way for you to change it.

Casey:Tell me about an example of something somebody built that made you say, “This is the promise of what I’m doing, realized” — the equivalent of that early moment with chatbots, when you saw the pieces coming together and how badly people wanted it, even though the technology was primitive.

Eugenia: A couple of things from my personal experience. I built this weightlifting tracker — I’d been tracking my gym workouts in Notes, which I found out a lot of people do. We make all of our apps agentic by default, and it started talking to me after my workouts, giving me some pointers on how to improve them. So I said, “Now also talk to me during workouts, as I’m logging — tell me what I can do as the next exercise.” And all of a sudden this app just felt so much more alive, and so much better than even a really fancy-looking app off the App Store, because it was smart. And not only that — it was also connected to my Apple Health, it was connected to my other apps, so all of a sudden it had a lot more knowledge about me. That was really a magical moment.

Another one: we have a few apps for our team. Our design engineer, Alex, makes lunches for us at the office every day, so we made an app where he puts up the menu for the week, and we can all vote and comment and say stuff — “Oh my god, these poke bowls were so nice.” It was just a little bit magical, because it created another way for us to bond more as a team.

To me, the really important thing is that today we have AI that lives separately in a chatbot interface, and then we have apps on our phones, and everyone’s debating: okay, MCPs or APIs — how are they going to communicate? But really, we should not have that distinction. Every agent or agent skill should just be an app, because a normal, regular person will never understand what an agent skill is, and no one’s going to go read Markdown files on GitHub. Instead, they can totally understand: oh, it’s just an app that looks at your inbox, and whenever there’s a new email, checks whether it’s an important one and sends you a quick summary. That is super easy to understand. If I tell you it’s an email agent that triages your inbox — “here’s the Markdown file, go figure it out” — that’s hard to understand.

Casey:In a world where everyone can make their own software, what does it do to the value of software that other people are selling — SaaS companies, for example?

Eugenia: The biggest problem with vibe coding is that no one’s going to use other people’s apps if those indie developers own the backend and the data. There’s just no way — even for consumers, let alone for businesses. If I build an AI therapy app on Replit and say, “Casey, use my fantastic AI therapy app, here you go,” you’re like: okay, well, Eugenia can read all my logs. [And so you won’t use it.]

And I don’t even need to be a bad actor. Maybe I just forget to maintain it, and then all your therapy sessions go away. Or I’m bad with security, and all of that is exposed to everyone. So the only way for people to share their personal software is to build it on one platform, where all the backend stays in one place, and the platform is responsible for security, the social graph, privacy, maintenance — the apps will never go away. And for B2B, it’s kind of the same premise.

Casey:So what is the sweet spot? If you project a couple of years into the future, what is the mix on my phone of apps that other people made and apps that I made bespoke for myself?

Eugenia: I think the only big, big apps that will stay are the ones that either have network effects — the big social networks, of course — or that have basically an offline business behind them, like Instacart or Uber. You’re not using those for the software, obviously. But everything that’s just software, I think, will go — especially all the subscription apps, the long tail of the App Store. That is going away. There’s just no need for any of it — it’s already barely working. If you really think about subscription apps — if you take out dating apps, social networks, and games, just the pure software — there’s only Duolingo that actually ended up going public. Nothing on the App Store that’s purely software really became a huge, huge business.

Casey:Would you be willing to name a name, or maybe a category, that you just think is actually in a lot of trouble here?

Eugenia: Subscription apps with low retention. Fitness apps, calorie trackers, sports apps, meditation apps — pretty much every app from that lifestyle and health and fitness category. They’re not providing a lot of value. If they have low retention, that means they’re just selling stuff during onboarding — that’s the name of the game for most of these apps — and then people just leave and never come back. Instead of that, I think people will want tools that are a lot more agentic, smarter, and tailored to them, and that they can use with their friends immediately.

Casey:So I used Wabi today — I made a podcast question evaluator. And I’ll give you a bit of gentle product feedback. The app looked very beautiful, but the keyboard was floating over the UI element to submit the question. I said, “Hey, the element is covered,” and it said, “Okay, I’m going to fix that” — and then it didn’t really fix it. To me this speaks to the challenge of DIY software. What has been your experience as you’re trying to bring people along? Do people have the patience to say, “I’m going to stick with this and figure it out,” or do they hit that limit and think, “I’m just going to ask ChatGPT”?

Eugenia: That’s a great question. When we started a year ago, on our evals we had 10 to 15 percent quality, which was: pretty much nothing’s working. So we had to build a lot around it. By November, it went to 75 percent, and now it’s probably at 80-something. And with our public launch we’re actually moving away from React Native to web views, and there we’re seeing closer to 90 percent. So I think that’s just going to be solved — it’s just a matter of time. We’ve seen the cost go down dramatically, the speed improve dramatically, the evals go up dramatically. Compared to Replika — where, in 2016, to think we would have meaningful conversations with computers was really crazy — to think that developing mini apps on the go will be solved in the next year? It’s a safe bet.

And what we figured out is that people forgive when it’s theirs. My weightlifting tracker is not the most perfect one, but it’s mine. I came up with everything. I’m very proud of it. It’s like pruning your own garden — we’re so proud of our kids.

Casey:That’s very real. When I’ve used other coding tools to make little tools that I use at Platformer, you do have a sense of pride, even though all you did was type in the box.

One word that gets used a lot to talk about what you’re doing is “democratizing,” right? You’re taking something that used to be the province of an elite, and you’re putting the tools into lots of people’s hands. There are many questions right now about the near-term future of software engineering, given that tools like yours exist. You are somebody who employs software engineers. How are you thinking about that question?

Eugenia: I guess there are two sides of it. First is the beauty of the idea that everyone can build — because up until now, there were maybe 6 million Android developers and 4 million iOS developers in the world, and billions of people using these apps. That’s a real mismatch. Instead of that, now everyone can be that person. And I do think there’s something beautiful in how it’s a little easier to create software than to make content — because one could argue, well, you can make great YouTube videos or Instagram stories. But there, if you look better, if you’re richer, it’s easier for you to do these things. With an app, it’s truly the quality of your idea. Anyone can create anything, and I like that a lot.

But the second part of the story is the questions about jobs. Compared to Replika, one of the reasons I wanted to start a new company was to work again with a team of 10 to 15 incredible people, instead of 100-plus people. Because now it’s just crazy how expensive it is to hire another person if you get it wrong.

Ten years ago there was this article about “below the API” and “above the API” …

Casey:Tell me about it.

Eugenia: When Uber and the on-demand economy were really happening, the idea was that you should stay above the API. Below the API means you’re working a job where the API tells you what to do — you’re an Uber driver, and an algorithm tells you what to do. And then there are people above the API — the software developers at Uber HQ who are developing the algorithm that will tell the driver what to do. So the whole idea was: stay above the API. And now it’s: stay above the AI.

But before, you could hire a 10x engineer — incredible — but you could also hire a 1x engineer,. and okay, the difference is 10x, whatever. Now, either you hire a person who is incredible at coming up with stuff and spinning up all the agents and doing the work — you’re hiring a 1,000x person — or you hire just some person who’s going to take up the time of the 1,000x person, and it’s really expensive. So hiring a not-so-great person, or a junior person, becomes extremely expensive — and completely unsustainable for a startup. And that, I think, is really hard.

That’s really bad news, frankly. I don’t have a solution. I think tech probably needs to create a better narrative for how this is going to go. I think the crazy protests around jobs and AI are going to start happening. We live in this very optimistic city, where it’s all about future, future, future — but as soon as you get out of here, it’s pretty scary. People are really struggling to find jobs, and I think this can only get worse.

Casey:How justified do you think that fear is? Do you think that two years from now there will be more software engineers, as we know them today, or fewer?

Eugenia: I think it’s a super justified fear. And I don’t believe in this “oh, it’s just another technology, and we’ll have even more jobs” line. People say, “Radiologists still exist!” I’m like, yeah, but I’m not hiring people anymore for these junior jobs.

Casey:First of all, thank you for saying what you just said. When I’ve talked to other folks in this series, there’s been a lot of reluctance to say, “I think there are going to be fewer software engineers.” Basically to a person, everybody has said: I think there’s going to be more — or maybe we won’t call them software engineers, but we’ll have more “builders.” It sounds like you started this company assuming maybe it will never be the size of your previous company, because you’re just not going to need as many people.

Eugenia: Yeah, I really believe that.

I think two things need to change. We’re still building the software of the past using the tools of today and the future. So we need to think: what’s the software of the future? How can apps change? We don’t need the same old apps and the same old distribution platforms operating this way when you can spin up an app in seconds.

And then the second question is: we should really think about a new type of company building. It’s almost like everything changed. For example, Figma designers — that is definitely going away. It’s just completely crazy to design everything, mock everything first, and then go develop it, and then test it and iterate. Of course everything should just be built at the same time.

I do think that right now, if you’re building a startup — specifically an application-layer startup like ours — you probably need 10 to 15 people, but absolutely insane people. And in order to attract them, because so many big companies are trying to get them, you need to change what you’re offering. You’re not going to attract them with 0.1 percent of equity and whatever the startup salary is. So we’re trying to do it differently.

I’m a big soccer fan, so I’m like: okay, let’s try to do a soccer team, where there are players on the pitch and there’s the back office. What are the most important roles for us? Let’s make them players on the pitch. They’re the team. Let’s give them the fame. Let’s give them a lot more ownership than employee number 15 would usually get — all 10 to 15 will get very meaningful, sizable equity grants. It’s a relatively flat hierarchy, but they need to be absolute superstars. And because you’re able to give a little more — pay them a little more, give them fame and ownership in a way that not a lot of other startups can — you create this incredible team on the pitch.

And everyone who is just doing one thing — maybe we need someone to deal with accounting, or legal, or motion design — we hire them as contractors, even if they’re full time. We want the top people there too, but that’s part of the agreement: you guys are coming in to fill a role, and the founding team is the founding team. And the people who put on a jersey with the name of the company — we want them to be active on socials, we want them to put their names out there.

Casey:And to cook lunch.

Eugenia: Cook lunch, yeah — everything. But that allows you to hire really top-tier people, not just as a first or second employee, but even as employee number 15. And I don’t think you need more than 10 to 15 people to build a billion-dollar company.

Casey:So in this moment, it’s possible to build a billion-dollar company, and you don’t need more than 10 or 15 people.

Eugenia: Well, some people are trying to do it with one.

Casey:I imagine some folks sitting here are thinking: Eugenia, I would love for someone like you to consider me insane, and a superstar, and worthy of putting on the jersey. What does that mean in practice? Has the skill set changed? What do people actually need to be able to do in a world where maybe there are only ever 10 or 15 seats at this company?

Eugenia: It really depends, because we have designers, product people, generalists, engineers. When it comes to engineers, it’s either really incredible generalists or people who are super good at that one particular thing. For example, Swift — it’s very hard to find a fantastic Swift iOS engineer, and we went through, I think, 120 people recruiting one, for our second-highest person. Because the question is always: will GPT-6 replace the person I’m hiring? And if the answer is maybe yes, then it’s an extremely expensive hire for us — it’s better maybe not to do it, because we’ll spend more time coaching and rewriting. But for everyone on the team, I think it’s agency, product intuition, design taste — whatever your specialization — and not being an asshole. Three very important qualities.

Casey:I think I understand what you mean by every one of those, but agency could mean a lot of things. What does a high-agency person look like at your company? What are they doing?

Eugenia: Well, Alex is one.

Casey: I think we can all agree Alex is extremely high-agency.

Eugenia: But frankly, I really think management at that stage is almost counterproductive, so people need to figure out what they do. We also build a lot of agents internally that are actually managing our company. But it’s people who can decide what needs to be done, go get it done, and push it to production. That is what’s needed. Ideally, you need a few generalists who can do it all the way, and some specialized people who are very good at backend, very good at frontend, polishing the stuff that they’re building. But you really just need people who know: okay, this needs to be done — quickly agree on it, and just go get shit done. If someone needs to go somewhere and agree, and then mock something up, and then develop it — you’ve already lost, because everything’s moving so quickly. There’s no time for that.

Casey:So being able to initiate a project and get it done without much help along the way — this is a core skill that you are hiring for.

Eugenia: Yeah. Get shit done. Also known as agency.

Casey:Last question. You’ve talked a little bit about your concerns about these new times that we’re moving into. Is there anything out there that is making you optimistic about AI and jobs in the near-term future?

Eugenia: The idea that we can all be creators, and can channel our creativity a lot more — can build stuff that before was constrained by developers or designers. I think that’s cool. We spend so much time on our phones using other people’s apps, doing what other people decided we should be doing. It would be really awesome if we could build stuff that would make our lives better. To me, that really is the way to ultimately connect with other people — use apps with friends, use apps with family, use apps with people you didn’t really know before. To me, that’s the beautiful part of it: all these new opportunities that are going to open up. And I think this is probably the first time where the iPhone is somewhat fragile. Maybe there is a way to build a better operating system that’s more serving us, versus serving companies through the apps that they built.

OpenAI is poised to automate one of advertisers’ most laborious tasks: ad creative.

Over the past four months of its ad pilot, OpenAI has required advertisers to upload the creative they want to submit, while the platform supports ad delivery. But now, OpenAI is going one step further in the process, by helping advertisers automate the mass production of creative, according to an updated section of its Ad Tools Term Document.

“OpenAI may make available AI-powered Creative Tools that allow you to generate, modify, transform, optimize, localize, or translate advertising creatives using Ad Materials,” the updated policy said.

That’s where OpenAI’s intention would stop. It has no intention of taking accountability for what the system produces. The policy states that the advertiser is “responsible” for reviewing the creatives and ensuring they are accurate and compliant where necessary.

“OpenAI is not responsible for errors, omissions, outdated information, or inconsistencies in Ad Materials or for Claims or losses arising from Generated Creatives that you approve or use,” the policy stated.

The move is hardly surprising, according to eMarketer’s principal analyst, AI in marketing and commerce, Nate Elliott. As he put it, it makes sense for OpenAI to throw AI at their ad operation.

“They know as well as anyone the power of AI for enterprise workflows; it’d be shocking if they didn’t tap that capacity for something they hope will become a major source of revenue,” he said. “And if they’re trying to make billions selling this type of capability to other companies, then they’d better very well eat their own dog food.”

It would also make it more competitive. Every major platform has spent years automating more of the buying process, which has made creative the last real variable. The logic being that once algorithmic optimization took over media buying, the bottleneck shifted upstream to creative. Platforms had a structural incentive to close that gap. More variants mean more auction signals, more liquidity, and ultimately more revenue.

“Marketers are moving faster than ever, and having proven creative assets ready to deploy lowers the barrier to experimenting with new advertising channels like ChatGPT,” said Brian Quinn, president and general manager of AppsFlyer. “But the real test will be campaign performance. If OpenAI can help brands launch seamlessly, demonstrate measurable results, and shorten the path from testing to scale, advertisers won’t just come back. They’ll commit larger budgets and make ChatGPT a meaningful part of their media mix.”

The creative tools aren’t the only update to OpenAI’s growing ad suite.

The AI platform has added conversion tracking for app installs and app opens, according to screenshots verified by Digiday. Ads for apps is a major category in online marketing, so laying the groundwork to track measurable actions such as installs, opens and purchases, would not only attract app marketers, but also provide OpenAI with another justification for more ad spend. And given how fast things are moving, the company clearly expects more ad dollars to start trickling in, having updated the daily ad budget from $100 to $200.

These latest updates show that OpenAI is moving beyond just selling inventory, toward building the complete infrastructure advertisers expect from mature platforms. Having the ability to produce creative at scale helps to solve the problem of having enough creative to feed the AI systems, while advancing conversion tracking helps to prove that those ads drive outcomes. And ultimately, these additions represent another step toward OpenAI turning its four-month old ad pilot into a fully-fledged ad business.

Your next breakout creator might already be on payroll. Here’s how to spot them before your competitors do.

In June, Starbucks said it would turn its baristas into paid TikTok creators. Through a program it calls Green Apron Creators, the company is now the first brand piloting a custom Creator Network inside TikTok, sharing content briefs and ad revenue with staff who post. Starbucks says its employees already post on social media at three times the rate of workers at similar chains.

This isn’t a one-off stunt. Employee-generated content, or EGC, is becoming a real strategy at companies of every size, and it’s the cheapest creator talent you will ever find. If you run a startup, the person who can grow your audience might already sit three desks away.

Look at the companies already doing this

Starbucks isn’t alone. Dell runs an internal ambassador program built on a certification it calls Social Media University, with roughly 1,200 trained “champions” posting across 84 countries.

Sprout Social built one too. It grew from six employees to about 100, and in 2025 those staff creators drove nearly 30 percent of the company’s video impressions while making up less than 8 percent of its content.

Look at how these companies are leveraging their employees. What type of content are they making and where? I’m the brand face for the creator vertical at the company I work for, so I appear in social content, as a host in our webinars, a coach in our programs, etc. Leverage faces as recognizable assets that bring you brand equity.

In the US alone, eMarketer expects sponsored social content spending to pass $10 billion. And more of it goes to smaller creators every year. eMarketer expects micro and nano creators to claim 45.5 percent of influencer marketing spending in 2026.

Your employees are the ultimate nano creators: credible, niche, cheap and already on payroll.

Bet on trust, because that’s what’s winning

Polished ads keep losing ground. People believe other people now. Sprout Social found 40 percent of consumers discover products through employee content, and that climbs to 61 percent for Gen Z.

Audiences are also tiring of the influencer machine. In a June 2025 Clutch survey, nearly half of consumers said they hadn’t bought a single product an influencer recommended in the past year.

When your employees talk about why they like working for your company, shopping at that company, showing their own dollars being invested back into the company, that builds a level of confidence a random influencer can’t.

Find the employees who already act like creators

Start with the people who want it. Look for who already posts about work on LinkedIn or TikTok, who co-workers go to for ideas, and who shows up for culture initiatives. Don’t draft anyone. Forced content reads as forced, and that kills the entire point.

Your best sign is someone who can take a rough script, make it sound like themselves, and hand back a finished video without much hand-holding. That person is ready to scale.

Treat them like talent, then cover yourself

Give your creators real support. That means a mic, a tripod, coaching and actual pay. Paying them matters more than founders think. Sprout Social found 61% of consumers believe brands should compensate employees who promote them, so set a model before someone goes viral and feels used.

Then handle the legal side. The FTC requires employees to disclose that they work for you, clearly and inside the post itself, not buried in a bio, and each violation can cost up to $53,088.

One last guardrail: employees can leave and take their followers with them. Keep your brand account resharing their work so the audience belongs to the company too, not just the person.

You don’t need a Super Bowl budget to win attention anymore. You need a few employees who love what they do and a phone. The brands pulling ahead right now already figured that out.

Anthropic has started rolling out multilingual support for Claude Voice Mode, with users spotting new language options.

A new Push-to-talk mode is also appearing for some users, offering an alternative to the existing hands-free conversational experience.

Anthropic may be working on something bigger for voice interactions, as a mysterious phone-call-style icon has surfaced in the latest iOS build.

We recently reported that Anthropic was preparing a significant upgrade for Claude’s Voice Mode, including support for multiple languages and a new Push-to-talk option. At the time, the evidence pointed to these features still being developed behind the scenes. Now, it looks like at least some of those changes are beginning to reach users.

An X user going by Evinstein recently shared a screenshot of an updated Claude Voice Mode interface and didn’t hold back on praise, claiming the experience is “100 times better than ChatGPT.” That’s obviously a subjective take, but the screenshots do offer one of the clearest looks yet at the incoming changes.

The updated Voice settings show support for additional languages, with Spanish (Latin America) enabled in the example shared online. Users can also switch between two different ways of interacting with Claude. The first is a traditional hands-free mode that allows for a more natural back-and-forth conversation. The second is Push-to-talk, where you press and hold a button while speaking, then release it to send your message.

Evinstein’s post was later quote-tweeted by TestingCatalog, which previously uncovered references to these upgrades before they surfaced publicly. According to TestingCatalog’s post, the multilingual rollout appears to have started on Claude’s mobile apps, though availability remains inconsistent. That means some users may already have access while others are still waiting.

Interestingly, TestingCatalog also spotted a new voice-related icon in a recent iOS build that resembles a phone call button. Anthropic hasn’t explained what this icon does, but it raises questions about whether the company is preparing a more phone-like conversational experience in the future. For now, that’s purely speculation.

The new Voice settings are already live on my iPhone’s Claude app, including the option to choose between Hands-free and Push-to-talk modes. I also found support for a much broader language selection, including German, Portuguese, Chinese, Japanese, Russian, and Ukrainian, among others.

That said, the mysterious phone-call-style option hasn’t appeared on my device yet. Based on what we’re seeing so far, Anthropic might be rolling out these additions gradually rather than flipping the switch for everyone at once.

If you’re curious whether you’ve received the update, open the Claude app, tap your profile picture, then tap settings, and open the Voice section. If the rollout has reached your account, the new options should be waiting there.

Sometime this spring, AI stopped being a passive tool you pick up and started becoming an active system that runs in the background.

For about two years, most of the AI I saw at conferences and in companies I work with fell into a category I’d call “cool demo, now what?” (I’ve written before about the non-obvious ways tools like GPT change the game.) Someone shows you a dazzling thing the technology can do, everyone applauds, and then Monday arrives and nothing about how the work actually gets done has changed.

That era is ending, and I don’t think enough people have noticed.

Sometime this spring, AI quietly crossed a line. It stopped being a passive tool you pick up and started becoming an active system that runs in the background. Recent reports describe autonomous agents that can manage and execute multi-step tasks without a human babysitting each step. One phrase from the research stuck with me: AI is moving “from demo culture into the operating system” of small companies. Not the flashy part. The plumbing.

That shift changes the question I think every leader should be asking. For two years, the question was, “What can this tool do?” The better question—the one that actually predicts whether you’ll get value—is: “What have we built around it?”

Run the co-worker test.

For each AI tool in your company, ask: is this something a person occasionally picks up, or a system that runs whether or not anyone’s watching? If everything is still in the “occasionally picks up” category, you’re stuck in demo culture and leaving the real value on the table.

Build the guardrails before you build the autonomy.

The big enterprise vendors are racing to turn safety, permissions, and audit trails into product features—because an unsupervised agent with the wrong permissions is a disaster waiting to happen. Before you let an agent act on its own, decide exactly what it can touch, what it must escalate, and how you’ll review what it did. Write it down on a single page. It may be the most valuable document you create all year.

Pick the handoff, not the takeover.

The mistake is trying to automate an entire job. The win is automating the handoff—the agent does the first 80 percent, then hands a human the 20 percent that needs judgment, taste, or care. The goal isn’t to replace your people; it’s to hand them the hard, human work with the easy stuff already cleared away. That’s not a smaller job. It’s a better one.

The goal was never to remove the humans. It was to remove the parts of work that were beneath the humans. We spent a century asking people to do robotic work because we didn’t have robots. Now we do. The opportunity isn’t to do the same work faster—it’s to finally let people do the work only people can do: the caring, the creating, the connecting—and let the quiet co-workers handle the rest.

The demo era is over. The operating-system era has begun. The only question that matters now isn’t how smart your tools are. It’s what you’ve had the discipline to build around them. Ask yourself the co-worker test today. The companies that answer it honestly—and then build the boring infrastructure—are going to look unrecognizable, in the best way, a year from now.

“Over the last 12 months, we’ve seen a flurry of [media advertising] activity from outside the retail sector,” EMARKETER analyst Sarah Marzano said on a recent episode of “Behind the Numbers.” But it’s not just advertising that’s shifting, younger consumers are actively seeking ways to disconnect from their devices and engage in physical experiences, prompting brands to rethink how they reach audiences.

This surge reflects a broader cultural shift as Gen Z and Gen Alpha trade digital feeds for real-world connections.

Quitting social media

Over half (52%) of Gen Zers tried quitting or cutting back on social media in 2025, placing it above fast food, sugar, and alcohol, according to November 2025 Check My Insurance data.

The desire to disconnect is clear, but execution remains challenging. Nearly 60% of Gen Z say social media has had a negative impact on their generation, according to 2024 Harris Poll data. Just 17% of Gen Z have never taken any steps to limit their usage, with the majority attempting to reduce screen time through unfollowing accounts, deleting apps, or disabling notifications.

The addiction is real, but so is the awareness.

“It’s an addiction, but it’s also inescapable because that’s the way in which we function with the rest of the world now,” said our analyst Paola Flores-Marquez. For Gen Z, social media serves as entertainment, discovery, communication, and work—all in one device that lives in their pocket.

The challenge of actually logging off

Despite widespread desire to disconnect, true digital detox remains elusive. Between smartwatches, Oura Rings, and other wearable technology, “there’s really no such thing as logging off anymore,” said our analyst Suzy Davidkhanian.

Logging off increasingly means supplementing digital habits with analogue activities rather than complete disconnection.

“I think Gen Z-ers are, well, again, Gen Z-ers are a majority adults, and so I think now they have the means to seek out and invest more in physical hobbies now,” Flores-Marquez said, citing pottery classes and in-person events as examples.

Retailers and consumer brands are responding to digital fatigue with physical activations and community-building initiatives:

• Levi’s operates tailoring and customization studios where customers can learn DIY techniques and personalize their clothing

• L.L.Bean launched its fifth annual “Off the Grid” campaign for Mental Health Month, featuring limited-edition analogue totes and customizable outdoor gear

• Ulta Beauty hosted a concert for loyal members at a major stadium

“Stores are 80% of sales,” Davidkhanian said. “Absolutely retailers and brands have to find different ways of getting people off their couches and into stores.”

These activations offer brands direct consumer insights in real time.

“There’s the added benefit of actually understanding your audience in real time, you know, getting all those insights, being able to connect at that level without having to wait,” Sevilla said.

Tech platforms and the problem

Even digital platforms are encouraging users to spend less time scrolling. Pinterest is positioning itself as a place to find inspiration online so people can live offline, while dating app Bumble is ditching its swipe feature in favour of AI-driven matchmaking to combat Gen Z dating app fatigue.

“The faster that they jump on acknowledging that and sort of encouraging more responsible usage, the faster that they either retain or regain consumer trust,” Flores-Marquez said. “Because right now everyone’s feeling like it’s kind of predatory.”

YouTube Shorts limits viewing time for younger users, and various platforms now offer tools for parents to restrict engagement.

“They’re doing that to avoid the liability, especially since there’s clear connections to mental health,” said our analyst Gadjo Sevilla.

As AI takes over from Google search, the thing that used to draw people to your creative work is disappearing fast. Here’s what’s happening, and how to respond.

At Cannes Lions 2026, Pinterest said something that should stop every creative in their tracks. Alongside a suite of shiny new AI advertising tools, the platform offered a candid description of where the whole industry is heading.

The web, it said, is moving “beyond the traditional search-and-click model toward a more conversational and generative web,” where brands now compete “not just for attention, but for recommendation, relevance and action”. That might sound like a boringly technical sentence, but buried within it is something very profound that affects every creative working today.

Because what it describes isn’t just a change in how Pinterest sells ads, but a fundamental change in how people find information and inspiration online. And if you’re a creative, the implications for whether you actually get work in future are huge.

Discovery is being dismantled

Until recently, the web gifted creatives many ways to attract clients that didn’t demand a huge marketing budget. A portfolio site that ranked in search results for “editorial illustrator” or “branding studio Bristol.” Instagram, Behance or Dribbble surfacing work to people who’d never heard of you. A piece is getting shared, and the share carries your name back to your profile. None of this required paid promotion.

Now, though, every rung of that ladder has been sawn off.

We’ve seen the decline of organic search: on Google, your freelance or studio site now sits below ads, AI Overviews and big-domain content, making it close to hopeless in promoting your craft. Meanwhile, social algorithms have decoupled reach from quality. Feeds now reward volume, trends and posting cadence rather than the best work, and throttle creators unless they either pay or perform constantly.

And now, as the final nail in the coffin, agentic AI (where AI basically acts as your personal assistant) has removed the last thing the first two still left intact: the click that carried a person to your door.

Who wins and who loses?

Nowadays, when someone types “find me an illustrator who works in cut-paper collage for a children’s book”, AI returns an answer, not a list of links to explore. It decides who gets named, and there’s no way to influence it: no ad slot to buy, no SEO lever to pull.

And how does it reach this decision? AI platforms lean on aggregate signals: who’s already cited, listed, written about, and linked to. This favours the already-famous and the big studios with a deep web footprint, leaving the vast majority of smaller independents floundering.

It’s a virtuous circle for the former, a vicious one for the latter. The visible gets recommended, and the recommendation makes them more visible. The talented new graduate with a thin online presence isn’t in AI’s field of view, so they stay invisible forever.

Pinterest’s new Ask Pinterest app captures this dynamic perfectly. It’s designed, the company says, for “more conversational, complex, multi-step decisions that don’t fit neatly into a single search”: planning a dinner party, furnishing a room over time, finding a gift that feels personal. Truly, it sounds like a great experience. But there’s a trade-off, and it’s a biggie. When answers arrive without a source, the source no longer matters.

So what should you focus on instead?

Pinterest is changing

Be a category of one

In this shiny new world of AI, you can’t optimise your way into a recommendation, the way you once keyword-optimised a website. Recommendation runs on reputation signals that a system can read: being named in other people’s work, on lists, in interviews, in the press, and in collaborations. So the answer for creatives isn’t to play the algorithms harder. It’s to become the name people and systems already trust enough to surface.

One part of that is to own your relationships. A newsletter list, for example, is a direct connection that no algorithm can intermediate away. A community of people who’ve chosen to hear from you isn’t subject to a platform’s recommendation logic. Look at how designers like Liz Mosley have built something genuinely resilient: a website, a podcast, templates, resources; an audience that actively follows her work rather than stumbling across it.

Another is to get cited and named, because getting talked about (positively, of course) is the new currency. This means leaning on the channels no algorithm can gatekeep: word of mouth, referrals, events, and real rooms. And in your work, aiming to be a category of one, with a style so specific it gets requested by name rather than retrieved by attribute. The creatives who get asked for by name are the ones that AI can neither replace nor substitute.

Lee Brown, Pinterest’s chief business officer, frames it this way: “The future of discovery won’t be driven by keywords alone. It will be shaped by context, taste, and trusted recommendations.” He’s describing his platform’s perceived advantage. But he’s also, accidentally, describing yours.

Context is where you work. Taste is what you’ve spent years developing. And trusted recommendations? Those come from people who know you and what you make, not from a system optimising for engagement.

Uncertain future

One last thought. If the systems doing the recommending keep starving the independents who make the original work, they’ll eventually run short of anything worth recommending. AI will ultimately kill off its own supply of information and inspiration. Where that death-spiral leads us is anyone’s guess, but it’s best to be prepared all the same.

In the meantime, I’d advise you to start building those direct relationships. Make the work that can’t be AI-assembled from anything else. And above all, don’t wait for your web traffic to disappear before you start, because that could be too late.

AI disrupted the current job market—and created a long list of new roles with impressive salaries across tech, medicine, HR, IT, marketing, and more.

Artificial intelligence is disrupting the current job market, leaving a trail of corporate layoffs and workers scrambling to determine what positions will be safe in the future.

At the same time, AI tools are also creating a number of high-paying jobs that didn’t exist a decade ago, according to a new report from job search and career platform Ladders. The survey looked at data from professionals earning over $100,000 a year and mapped the top 15 six-figure jobs that it says are worth considering.

“Most headlines frame AI as a wrecking ball aimed at our paychecks,” Marc Cenedella, Ladders’ CEO, tells Fast Company. “This study, however, shows [more than] 1.3 million new jobs have been created since the term ‘AI’ entered the mainstream vernacular, with many of those roles paying 56% above the rest of the pack.”

These jobs exist across industries including medicine, marketing, technology, human resources, information technology (IT), and cybersecurity.

Cenedella says the study’s real value is that it provides a map of the jobs that workers should invest their time in today, including a mix of new positions (chief listening officer, AI ethicist, and climate change analyst) as well as some obvious choices (SEO specialist, social media manager, and chief AI officer).

“The best job bets all share one trait: A human is managing the machine, not racing against it,” Cenedella adds.

AEO specialists and AI ethicists?

Cenedella says there is currently a high demand for AEO specialists and AI ethicists. But what exactly do they do?

As AI-generated summaries cut search in Google by 45% (even though the summaries are wrong 10% of the time), companies are adapting to the collapse in web traffic by investing in answer engine optimization (AEO) specialists, who make sure their original content appears in AI overviews or large language models (LLMs) like ChatGPT and Claude. These AEO specialists are the next generation of marketing and website professionals.

Alternatively, the need for AI ethicists will only continue to grow as AI agents make more autonomous decisions, requiring a human to verify that their output is accurate, legal, and fair. AI ethicists set policies for how companies can ethically use AI while protecting against data leaks and major mistakes AI agents can make, such as deleting 2.5 years’ worth of records.

15 high-salary jobs in 2026

Here is the full list of 15 high-paying jobs in the age of AI, as well as a salary range and degree requirements for each.

Chief AI officer — $200,000–$500,000 (bachelor’s degree minimum)

Influencer manager — $135,000 (no degree required)

AI ethicist — $70,000–$170,000 (bachelor’s)

Data protection officer — $118,000 (bachelor’s minimum)

Data scientist — $112,000 (bachelor’s)

Climate change analyst — $112,000 (bachelor’s)

Drone operator — $71,000–$100,000 (remote pilot certificate)

AEO specialist — $91,000–$180,000 (no degree required)

SEO specialist — $86,000+ (no degree required)

Social media manager — $74,000–$200,000+ (no degree required)

However, Cenedella adds that degree requirements shouldn’t be a main focus. “The smartest move a worker can make today is to stop treating a degree as the main thing that qualifies them and start building proof for why they should own a role instead,” Cenedella tells Fast Company. “Whatever your current job is, do a piece of it with AI, capture the result, and put it somewhere you can show it: A year of quietly documented results beats a degree program that won’t exist until you’re already too late to it.”

Jennifer Mattson is a Contributing Writer at Fast Company, where she covers news trends and writes daily about business, technology, finance and the workplace.. She is a former network news producer for CNN, CNN International and a number of public radio programsMore